Do you actually need an emergency fund?

If you’re reading this, you’re probably thinking one of two things:

- We definitely need an emergency fund, but we can never seem to build one up.

- It’s a waste to have money sitting in cash earning nothing, so we don’t keep a lot in our savings account.

Traditionally, an emergency fund is thought of as “3 to 6 months of expenses in cash”. So many people just go on accepting the advice without actually figuring out if that’s actually the case.

But even though people feel like they should have it, many of the clients I work with never seemed to make it there.

Sometimes it’s that they’re not sure how to get there. Other times it’s more about raising their financial standards to improve.

The question is, do you actually need an emergency fund?

We’ll break it down here and go through the pros and cons.

If you have a spouse, partner, or significant other, chances are you’ll have different perspectives on this, so we need to look at the math behind it and other psychological factors too.

I’ll take you through both sides.

Let’s start with what is an emergency fund.

Table of Contents

What is an emergency fund – Not just for the bad stuff

I know what you’re thinking, “Rob, we all know what an emergency fund is. You don’t need to explain it.”

Yes, we all know an emergency fund is a cash cushion for unexpected expenses like:

- Home repairs

- Auto maintenance

- Unforseen hospital visits

But we focus so much on the bad, we forget that the cash cushion can also be used for good like:

- You get invited to go on a fun vacation with friends (girls trip, guys trip, or couples’ trip).

- You discover that your kid lights up when they ____, and you want to support that passion.

- Your favorite music group or sports team is coming to town and tickets are pricey.

An emergency fund also allows you to be opportunistic and jump on something that could be great for you if you only had the money.

How many times have you said to yourself, “Ooo! This looks great! If we only had the money for it…”

Bottom line is that an emergency fund is a cushion for unplanned emergencies…and positive events too.

Why you need an emergency fund – The math behind it

I get this all the time:

“Why do I want money in the bank earning nothing? I’d rather invest it and make more on it.”

It’s tough to see all that money doing nothing when there could be other opportunities out there.

Let me agree with that thinking a little bit. Mathematically, there is some merit to it.

It’s the idea that paying your mortgage early won’t end up nearly as good as investing that extra money over the next 30 years.

Sure if you can earn 7-10% per year while “borrowing” at 4% you could end up in a better net worth position.

I can see that perspective.

But here are the two key assumptions made with that perspective that could be some flaws with that thinking:

- The money that would be flowing toward the mortgage is being invested…not spent

- That 7-10% investment return carries little to no risk.

When we’re talking about holding cash in case of emergency, it’s a little bit different than the “invest instead of paying down your mortgage” thinking.

Whether or not to hold cash in your emergency savings account comes down to two questions mathematically speaking:

- What are your options if you need cash but don’t have it on hand?

- What else would you do with that money if it wasn’t sitting in cash?

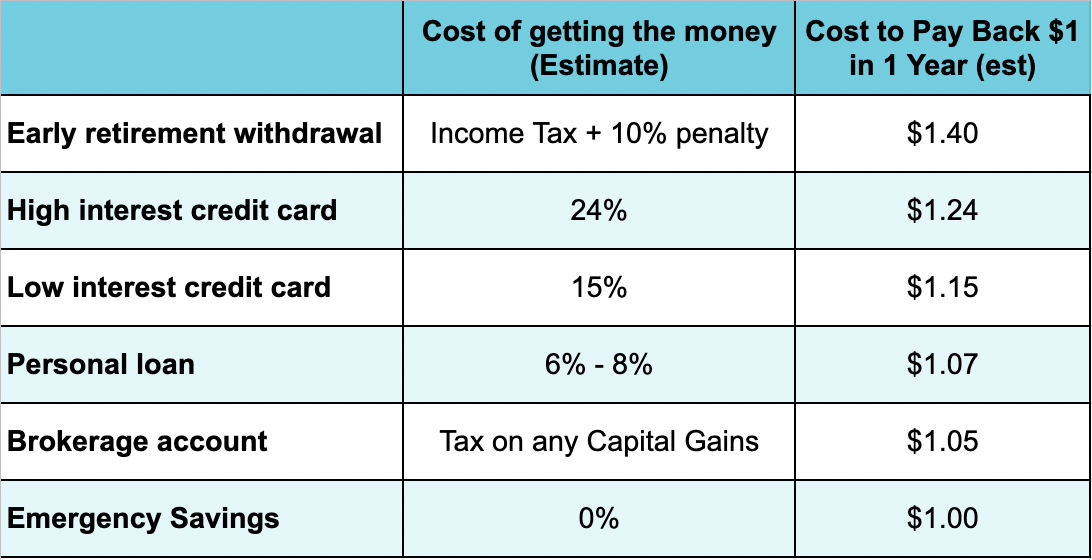

What would you do to get cash if you didn’t have an emergency fund?

Let’s say you have a $5,000 cost to cover from needing a new HVAC in your house.

If you have that money sitting in your emergency fund, you can simply pay it.

Ouch! It still hurts, but you’ll manage.

If something like this comes up that you have to spend money on and you don’t have it in cash, you have some options:

- Put it on credit cards and carry a balance.

- Get a loan to cover the cost or put it on a payment plan

- Pull money out of your brokerage account.

- Take money out of your retirement accounts.

Here’s a table that shows the potential cost of getting money from various sources:

Think of the interest rate on debt like an investment return you’re giving to the person holding the debt.

Someone’s credit card debt at 15% is the bank’s 15% return on investment.

Every extra dollar of principal paid down is like that money earning 15%.

But paying off debt is better than investing at the same expected return, because paying down debt gets you that return:

- Risk-free

- Tax-free

- Guaranteed

- Immediate

When you invest, there’s volatility and risk involved so it’s more efficient to find the same return with less risk.

That’s why paying down debt beats investing at the same expected rate of return.

(Plus, it frees up that monthly payment after it’s paid off and takes leverage/risk off the table.)

So the next question is, what can you expect to earn on investments?

What if you invested your money instead of keeping it in cash?

We could look at all sorts of investment products and services, but let’s stick with the stock market which has given the highest rate of return over a long period of time compared to other asset classes like real estate, bonds, etc.

The Vanguard Total Stock Market Index has returned a 9.9% average annualized return for the 20 years ended 12/31/2021 even though the market went on a tear the last 3 years of that time period.

That’s the return for an all stock portfolio, but most people have a globally diversified portfolio with some of the asset allocation to bonds and cash.

So let’s lower that 9.9% all US equity return down to 7%.

Let’s make some assumptions here to simplify the math before we look at the break even analysis:

- 7% is the return we’d make each year (even though we know the stock market is volatile and it doesn’t go straight up).

- Timing of when you’d take out the money doesn’t matter (which studies show it has a huge effect).

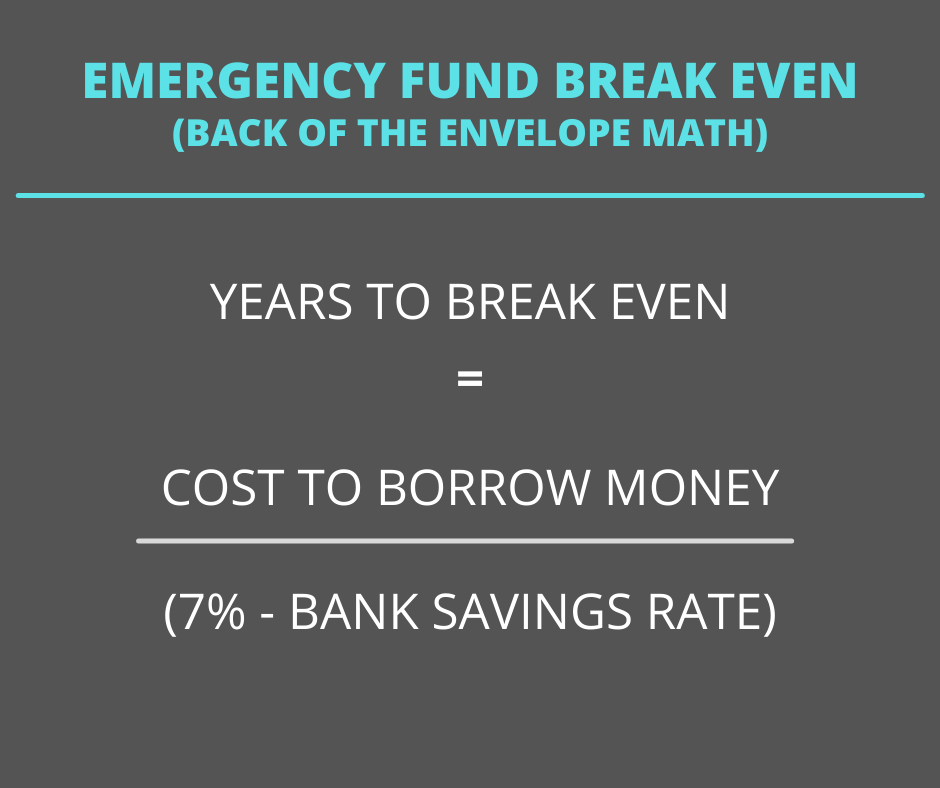

Emergency fund break-even calculation – Short-hand rule of thumb

We’re assuming the money is invested and earning 7% instead of sitting in the bank, and that you’d have to take out some sort of loan, debt, or withdraw from your investments or retirement accounts to pay for an emergency.

The super simplified break even calculation is:

Years to break even without emergency fund = Debt interest rate / (7% – bank interest rate)

So if you have to put something on a 15% credit card, then it would take 2 years of earning 7% to break even.

Think of this calculation as a short-hand rule of thumb, because this isn’t the perfect formula by any means. I’ll admit my flaws in this calculation:

- Market returns are volatile and using a long term average may be way off.

- We don’t normally have clarity on how long it will take us to pay back the debt.

- The amount we need to borrow is unknown in advance.

- The cost of paying back debt is lower if we’re making monthly payments that are paying down principal along the way.

We can always do a backward looking analysis to see if it worked out, but it’s hard to project in advance.

However, the lower the interest rate on the debt and the more predictable the future investment returns, the more this calculation will hold.

Math summary

If there’s one takeaway from this math portion, it’s that the sources to get cash can be very expensive if you don’t have the funds available.

That means the cash “sitting there doing nothing” is actually preventing you from having to take out money in a more costly way if you needed it for emergencies.

So in essence, that money in the bank has value well beyond the paltry interest rate.

Why you need an emergency fund – The psychology behind it

Phew! We made it through the math. Thanks for bearing with me there 🙂

As we know, finance is personal, so math IS NOT the only thing that matters.

There are other factors at play.

Think of it this way.

There’s a reason you spend money on discretionary things like vacations, dining out, grocery delivery and hobbies.

They help you relieve stress, take your mind off other things, and help you recharge.

Emergency savings provides a similar benefit.

Imagine you had to come up with $2,000 today but you didn’t have it in your bank account (we’ve all been there).

You’d have to think through:

- How will we pay for this?

- How long will it take us to pay it off?

- How much extra will this cost us with interest?

That can be stressful!

How will that carry into how you operate at work, with your family…with your finances?

It’s hard to focus and make the best decisions with that weighing on your mind.

Now think about if you had enough money saved to cover the cost and then some.

You might think, “This is not great, but…we got this!”

Having an emergency fund is like having the perfect set up to sleep well at night.

The mattress is comfortable, the room is at the right temperature, you have blackout shades, and it’s quiet.

Like that setup, the emergency fund helps you sleep better at night.

Just like taking a vacation, having cash on hand can help you feel energized and relaxed.

Do you need an emergency fund?

The answer is yes.

That is unless you’re a super duper financially savvy, analytical person who only sees value in numbers optimization and can operate without emotion.

(And your spouse, partner, significant other sees things exactly the way you do.)

Your emergency fund acts as your insurance.

It can keep you from having to make a costly financial decision.

Plus, it provides a sense of comfort psychologically, so you can operate without worry and distraction WHEN something unforeseen comes up.

Now that we’re all on the same page here, there’s one little problem.

Not everyone has one set up.

Why do people struggle to build emergency savings?

Plenty of people have trouble building an emergency fund, even if they agree with everything we’ve covered so far.

The biggest reason I see why people have trouble building an emergency fund is…wait for it…they have gotten used to not having one.

Even if your savings goal is to have one, we revert back to what we’re used to.

It’s like a thermostat.

When you have more money than you’re used to in your checking and savings accounts, we feel rich and that money somehow gets spent.

When you have less money, you somehow get yourself to make changes to get yourself back up to that number.

Your financial thermostat is set to the level that you’re used to.

The second biggest reason I hear people struggle to build an emergency fund is, “Something always comes up that sets us back.”

There are many stages of life and some come with much more challenges than others.

But what I’ve found is that some of these “things that come up” can be predictable. We just forget about them until they are upon us because these irregular expenses don’t happen every month.

Kind of like a kid’s birthday party, summer camp, planning a vacation, etc.

How big of an emergency fund do you need?

Not everyone needs the same amount. Some families can get away with having less than 3 months and others might need more than 6 months.

Here’s how to figure out if you should have a larger or smaller amount of emergency savings.

How complex is your life?

Someone who is single with no kids, no house or car doesn’t really have a major need for emergency savings as long as they have health insurance.

Not much can come up that will require having a bunch of savings on hand.

Conversely, the more components of life you have, the more likely you’ll have an unexpected expense.

If you have a house or a car, something will go wrong at some point that will require repairs of many thousands of dollars.

With kids, there will be plenty of bumps and bruises (hopefully very minor) that could require a trip to the emergency room. It could also be that they find a new interest, hobby or passion that you want to support and pay for.

More people and more stuff requires more in emergency funds.

How predictable is your cash flow?

If you have a super steady job with predictable income and a high certainty of staying employed, then the need for an emergency fund is relatively low.

One the flip side, if you’re self-employed and growing a fledgling business, month-to-month cash flow can be all over the place.

The same is true if you’re paid on commissions or tips.

Some months you’ll have to draw on a safety net, others you might have excess you can save.

A bigger cushion will come in handy when there’s a shortfall.

Dual income or single income household?

A dual income household is better protected if one person loses their job, because at least there’s still income coming in while the other is on the search for a new job.

But in a household with only one person earning money or if there’s a breadwinner, then the household finances are highly dependent on their job security. A job loss could be catastrophic.

A larger emergency fund should be considered.

What number makes you feel comfortable?

Going back to the psychological aspect, some people are more risk averse and feel better with a larger safety net.

There’s nothing wrong with holding more cash in your savings account if it reduces your stress and helps you perform better in life.

Although this shouldn’t be the primary factor in determining the size of your emergency fund, it should certainly be a factor.

How much do I need in my savings account for emergencies?

The conventional advice for emergency funds is to hold three to six months worth of expenses for unexpected events.

But more complexity, unpredictability and reliance on one income means skewing more towards six months of expenses or maybe even more.

Everyone should work towards having at least one months worth of expenses in the bank no matter what the situation is.

I personally like holding more money in the checking account, but you should do what you feel is best for you and your situation.

(Keep in mind, this is the amount in emergency savings BEFORE your paycheck comes in, not after.)

How to build an emergency fund

I often hear, “We just don’t seem to have money left over at the end of the month.”

It’s hard to build an emergency fund when you feel like you can’t save money in the first place.

There are definitely some great financial habits you can start to get there, but often all it takes is breaking down big goals into smaller milestones.

Then, the trade off becomes tangible and achievable between spending or reaching a financial goal.

For example, if you have $1,000 in the bank and need to get to $20,000 for a fully funded emergency fund, that can seem like a big lift.

But if you create other milestones in between both in terms of dollars and time frame, this not only helps keep momentum, it also helps you get used to adjusting your “thermostat” to a higher level.

In this example, I’d work on getting from $1,000 to $2,000 in savings over the next 2 months, then $5,000, $10,000, $15,000, then $20,000.

Figure out how much money you have left over to put towards this goal, but don’t start with a budget.

Start first by tracking your spending to see your starting point. Then figure out how much you have to start saving.

Plus, you’ll know your actual living expenses and how big your emergency fund should be.

Where do I put my emergency savings?

As long as it’s liquid in cash, it can be any accounts that you have easy access to including:

- Checking account

- Savings account

- Credit union

- High interest savings account

- Money market

I like at least one month in the checking account and the rest in a linked high yield savings account.

Where do your other savings goals fit in while building your emergency fund?

The three major milestones to meet in terms of saving, investing and paying off debt are:

- Have an emergency fund

- Being credit card debt free

- Take advantage of the full match from your employer retirement plan.

Stop and do nothing else until getting this financial foundation in place!

What would it feel like if you had no credit card debt, enough in emergency savings to be comfortable while also working on your long term investing.

Wouldn’t that feel so amazing?

You can either go with one of those at a time or pick 2 to work on at the same time.

Either way, any money set aside should go towards these areas first.

Do you need an emergency fund?

Yes, you need an emergency fund in almost all circumstances. Start saving up for one month of expenses.

Then build to the level you need based upon your comfort, complexity, and predictability of income.

The greater your complexibility, unpredictability, and monthly spending, the larger the emergency fund you’ll want.

Money affects our finances and also our stress and anxiety, so remember to take a holistic approach to your emergency fund calculation, one that encompasses the numbers and the emotional component.

If you want help figuring out how much you need or how to build yours up, I’m here for you.

Book a free session.