Get a raise by cutting your expenses

Have you ever thought, “If I could just make more money, that would solve all of my financial problems!”

No doubt it could, but have you ever thought about the other side of the coin? That cutting your expenses is like getting a raise?

It’s true!

I’ll take you through a few ways to reframe your thinking about expenses and how it compares to your income and your time spent working.

When I first thought about this, it blew my mind. Then I realized that other successful people are using this thinking too!

Now it’s time to let you in on the secret.

Table of Contents

How is cutting your expenses like getting a raise?

They say a $1 saved is a $1 earned, but that’s not entirely true.

$1 saved is BETTER than $1 earned.

Why is that the case?

Think about your income.

Ok, now think about your take home pay.

Are they the same?

Nope.

That’s because you have to pay taxes.

You actually have to earn more than $1 to save $1.

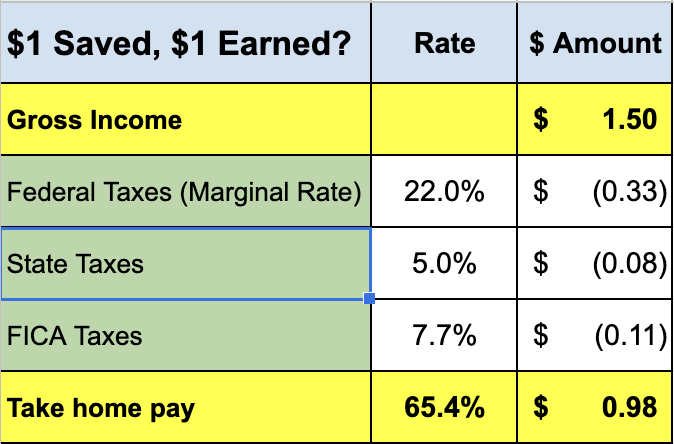

Let’s say your marginal federal tax rate is 22%, 6% in state & local taxes and 7.65% in social security and medicare taxes.

That means that every extra $1 you make, you take home $0.65 after taxes. Put another way, you have to earn about $1.55 to take home $1.

(For simplicity, let’s just say you have to make $1.50 to take home $1).

So if you want to spend an extra $1,000 per month, you need to earn another $1,500 per month or $18,000 per year.

So, let’s update the saying to, “$1 saved is $1.50 earned.” (image quote).

AND, this works in reverse, because if you spend $1 less, it’s like increasing your income by $1.50.

In other words, if you cut your expenses by $1,000 per month, it’s like giving yourself an annual raise of $18,000.

How to frame your expenses as income

Now that we know every dollar we save is better than a dollar earned, we need to shift our thinking about our how we think about spending money.

There are two options to reframe our thinking around it.

Let me just warn you. These options might shock you a little bit, but that’s kind of the point.

Option 1: Think about $1 spent as $1.50 earned

This is a real mind-warping exercise.

If you think things are expensive, convert them to how much you’d have to make to pay for them.

Add 50% to your spending to see how much you’d have to earn in order to pay for it.

Those streaming services at $7.99 per month, now it’s $12 per month.

Your $2,500 mortgage or rent payment means you have to earn $3,750 per month to cover it.

That $30,000 car is now $45,000.

Mind-BLOWN!

Obviously, this isn’t the most fun way to think of it, but at least you’re giving it the correct context, and reframing what something costs.

Option 2: Convert your take home pay your actual income

That six-figure income you make is nice, right? But, you actually only have a five-figure take home pay for every $100,000 you make.

Forget about your salary, it’s how much you take home after taxes that matters.

That’s what you have available to spend.

For every $100,000 you earn, you probably take home about $65,000 (about $5,500 per month).

When you make a budget, it’s better to make it based upon what you take home anyway right?

How long do you have to work to pay for it?

Now that you know how to convert your expenses into your actual income and we know $1 saved is better than $1 earned, it’s time to think about our spending in terms of…time.

You’ll want to convert your take home pay into how much you earn per week, day and hour.

Here’s how to do it:

Start with your take home pay and then divide it by:

- 4.3 for your weekly amount

- 22 for your daily amount

- 180 for a traditional 40 hour work week (or 4.3 x hours worked per week if you work more or less than that).

Let’s use some easy math here in an example using take home pay as a way to measure expenses.

This household is taking home about $8,800 per month after taxes.

If the average month has ~22 working days in it, so we can convert our spending into how long we’d need to work to pay for it:

- Week = $2,000

- Day = $400

- Hour = $50 (8 hour workday).

Once you convert your take home pay to time, you can then ask yourself:

“Is it worth me working (this amount of time) to buy this?”

Whether it’s the big ticket purchases or the little things that add up, you’ll want to look at your total monthly spending and see how long you have to work each month to cover each area.

Here’s what it could look like (chart or calendar)

- Housing costs: $3,200 = 8 work days

- Food & dining: $2,000 = 5 days

- Debt payments $1,200 = 3 days

- Car payments: $800 = 2 days

- Everything else: $1,600 = 4 days

Then annualize it (Calendar with exact dates)

- Housing costs: $36,000 = ~4 months (Jan, Feb, Mar, April)

- Food & dining: $24,000 = 3 months (May, Jun, Jul)

- Debt payments $14,400 = 1.6 month (Aug – mid-Sep)

- Car payments: $9,600 = 1 month (Mid-Sep – Oct)

- Everything else $19,200 = ~2 months (Nov, Dec)

You can break it down to weekly (M-F with hours 9-5) too if you want.

Take what percentage of your income your spending is, then multiply it by how many hours you work each day.

By the way, in this example, they are not paying their future self in the form of savings or investing.

This may not make you feel great, but it does highlight what you are ACTUALLY working for.

Hopefully this is shocking your system and motivating you to make some spending changes.

Where should you start?

Start by keeping track of your spending

If you really want to see how getting a raise or cutting your expenses could benefit your situation, it all starts with tracking your expenses.

We can all name the big bills, the housing payment and car payment, but how much are you spending on food, shopping, bills, streaming services, your phone plan?

Then you can ask yourself, “Is this worth my time and money or would I rather give myself a raise by spending less or cut my costs so I can work less?”

Bottom line, there’s no need to spend on things that aren’t worth it.

Start giving yourself a raise by getting rid of the spending that serves no purpose in your life.

Remember, you have to earn $1.50 for every $1 you spend on a streaming service you’re not using, the food you’re throwing away,

Then get rid of the excess spending on things you enjoy but are spending too much on.

DO NOT START WITH A BUDGET.

Start with first tracking your spending so you know where you can easily make these changes.

And then…

Have a plan for what to do with the extra money

Honestly though, none of this will stick unless you know where your money is going and have a plan of attack.

I see many people who get into the, “If I could just make more money…” mentality, but when they get a raise or bonus, it just goes right out the door because they haven’t taken the time to be intentional about it.

A lot of money can get spent quickly even if our intention is to save it and pay off credit card debt.

When you have a plan of what to do with the extra money, it will be more meaningful to you, and you’ll ensure that it doesn’t get squandered.

Supercharge your raise

Here’s where the numbers switch from being dreadful to…fun!

Here’s how to multiply the affect of giving yourself a raise.

There are two parts here: Making your spending count and deploying money to your balance sheet for max benefits.

Make your spending count

It’s ok to spend money in alignment with your values, priorities and lifestyle you want to live.

But you need to make your spending count, because once you spend it, that money is gone for good.

When you buy something, you are transferring your wealth to that company.

Think about it this way, the reason Amazon and Apple are two of the wealthiest companies is because so many people buy their products and transfer their wealth to them.

I’m not saying that’s a bad thing, because spending money is ok.

But, why transfer your wealth to a company when you either don’t use it, don’t like it, or think it’s only ok. Wouldn’t you rather build YOUR wealth with it instead?

Tthat’s why every dollar you spend should be intentional.

Think about what to spend money on to live your best life. Then keept the rest of the wealth in your pocket rather than making a purchase you don’t really care about.

Save money and multiply every $1 of it.

You can also supercharge your raise by deploying it to your balance sheet.

Paying off high interest credit card debt means that paying off an extra $1,000 actually turns your $1,000 into $1,200 immediately.

Flash back: Remember the $1 saved is $1.50 earned?

Well, a dollar saved is WORTH MUCH MORE than a dollar earned.

Cutting your expenses by $1,000 and putting that toward 20% credit card debt is like earning an another $1,800 rather than $1,500.

Investing $1,000 in an index fund and earning 7% means that it would double in 10 years, 4x in 20, and 8x in 30. (Thank you compound interest).

So every $1,000 you invest today could turn into $8,000 in 30 years.

If we apply the $1.50 multiple, saving $1,000 today is like earning $12,000 ($8,000 x 1.5) in 30 years.

Math and compound interest rocks, right? (Cricket sound).

Bottom line is that a dollar saved is WORTH MORE than a dollar earned

Ask for a raise too though 🙂

Asking for a raise can sometimes be intimidating, but if you’ve done your research and have external data and can demonstrate your value to the organization, then you may deserve a raise.

That one conversation can have long term effects on your perceived value in the marketplace, your career, and your personal financial situation.

Research compensation across the profession and job title and be prepared to show your performance and your value to the company.

There are plenty of great resources out there to help you there.

Need help cutting your expenses?

Now that we have a framework of why it’s important to save money, how do we come up with more of it over time?

Whether your goal is to save money, pay off debt, take a pay cut for a job that fits better with your stage of life, you’ll want to give yourself a raise by eliminating wasted money according to you.

I can help you find more money at the end of the month so you can reach your financial goals and live the life you want along the way.

Let’s start by having a conversation about simple things you can do today to make that happen.