10 Budgeting Questions: How to Spend Less While Enjoying Life

It sounds easy. Spend less than you make!

Yes, that’s an easy concept to understand, but we’re used to our habits, routines and lifestyle.

A budget makes us feel like we need to give it all up, stop spending money, and follow a rigid and restrictive process in order for it to work.

Plus, it takes a lot of time to take all of our expenses and put them in a super specific budget category.

But that is flat out WRONG!

Creating a budget is not all just seeing how many expenses you can cut.

Making a budget is all about giving you room to spend money on the things you enjoy while also getting rid of the stuff you don’t care about.

The first step in starting to budget is not getting right to the spreadsheet.

Start with asking yourself these budgeting questions. That will help you create a sustainable budget while helping you reach your short-term and long-term goals.

We’ll take you through questions to ask before you start budgeting, then do a budget review, and present some general budgeting FAQs.

Table of Contents

Questions to ask before you start a budget

Imagine looking at your bank statements and credit card statements and getting excited because it shows that your money was:

- Spent on things that matter to you.

- Going toward the best places to eliminate your money stressors and reach your financial goals.

It can happen!

The goal of a budget is to make every single dollar count.

Figure out what that means for you by answering these key budgeting questions.

What are your values and priorities as an individual, couple & family?

Don’t let anyone else tell you what a waste of money is for YOU. A waste of money is when you spend on things you don’t care about.

So let’s figure out what matters to you.

What are the things that help you become the best version of yourself, refresh & recharge, and that are just plain fun?

What values and priorities are important to you?

Identify these things in three areas: you as an individual, you as a couple, and you as a family.

Preserve spending in these areas to live your best life.

Make room for this in your budget.

What are your biggest financial stressors right now?

Where can your money flow to help relieve stress?

What part of your financial situation is taking up your emotional energy?

Is there a particular debt you want to take care of? Feel like you want more cash in the bank?

Budget money to get rid of it.

How much have you actually been spending over the last three to six months?

Many people set a budget that is doomed to fail, because they pull numbers out of the air and think they’ll just make it happen.

Past spending is a reflection of your spending habits. Changing them can be a challenge if it’s too drastic too fast.

Start by tracking where you have spent money. Reviewing your spending will help you identify the things that don’t fit in with the answers to the questions above and are a waste of money according to YOU.

What are the fixed expenses that would be hard to change?

Monthly fixed costs should be off limits to change at the beginning because they would require a drastic life change.

Your mortgage payment or rent (and the monthly bills that go along with it), tuition for the kids’ school, fees for their activities, and car payments are a perfect example of that.

Whatever you feel would be very hard to change, add up all of those expenses.

The expenses that remain will be the ones you have to work with.

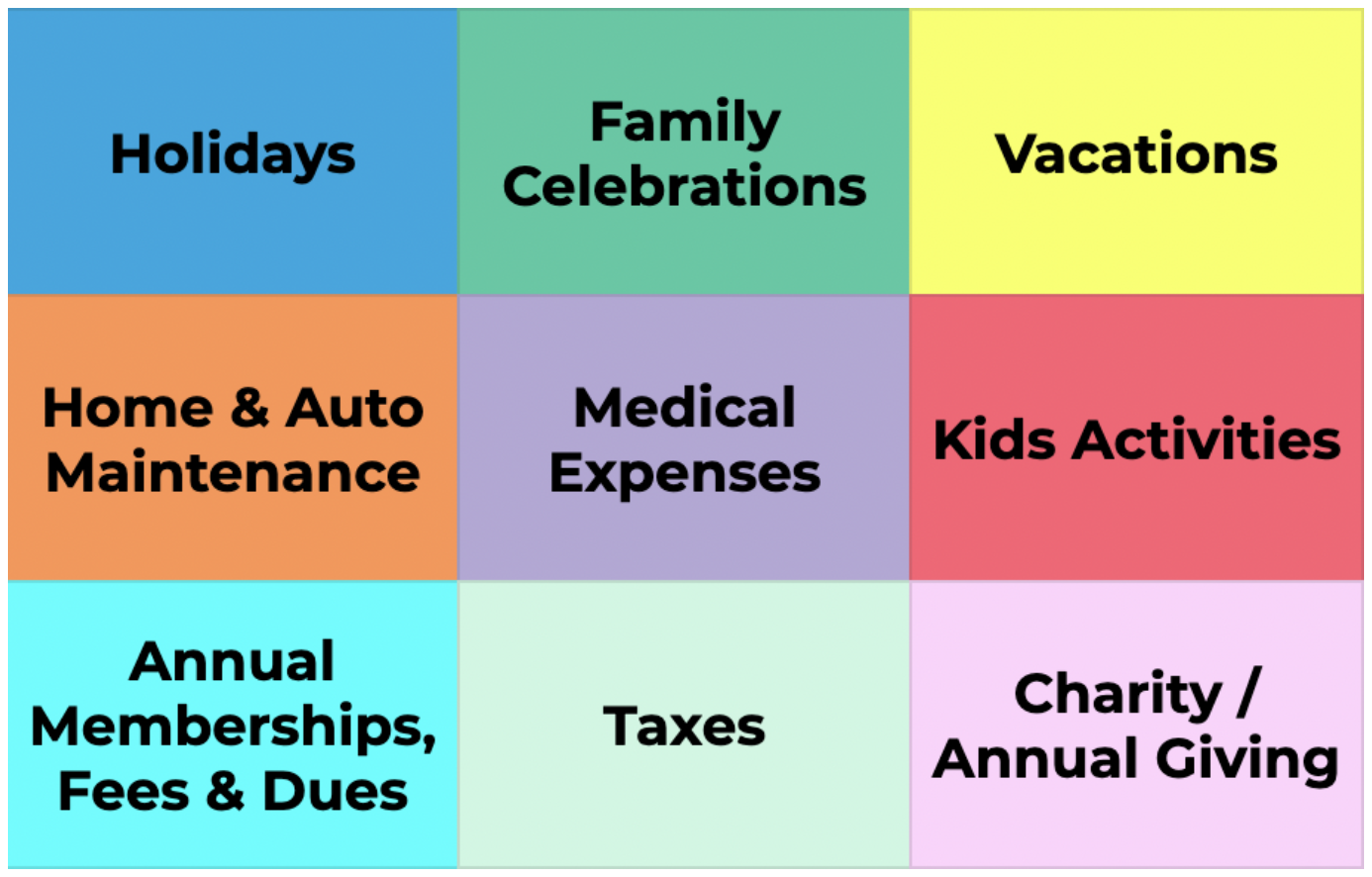

What are your irregular (but expected) expenses for the month?

“Something always seems to come up!”

These are the budget busters that happen every year, but we just seem to forget about them because they aren’t a monthly expense.

Things like the holidays come to mind first, but what about birthdays, anniversaries, other holidays throughout the year, summer camp dues, regular vacations?

Don’t let these things sneak up on you.

Putting together a list of your irregular expenses and budget for them.

What are your financial goals?

Trying to pay off credit card debt, build an emergency fund, or save for retirement?

Budgeting will help you get there.

Remember that needless transactions are transferring your wealth to someone else so make these dollars count!

Cut out the costs that you determine are a waste of money to make more room to reach your financial goals.

Spend on what matters and set aside the rest to your savings goals, invest for the future, pay down your debts and become debt free.

What is your take home pay?

Notice I said take home pay and not gross salary.

What matters is the money that actually enters your bank account.

If you run your own business or are self-employed, the income should be what you take from the company after taxes.

Create a method to calculate the taxes you should be withholding. You can work with an accounting firm or tax software if you need help with this.

Bottom line is that the income you put into your personal budget is not your salary. It’s your take home pay.

How would you want to spend the leftover money?

You now know how much is coming in, your fixed expenses, how much to put toward your financial goals. Now, what should you do with the extra money in your budget?

What other spending would you want to do that is aligned with your values and priorities or could help you alleviate the financial stressors?

Based upon what you know, how would you budget the rest of it?

What changes are we willing to make to make this happen?

The perfect budget where the numbers all fit together mathematically is not necessarily a recipe for success.

A budget doesn’t work unless it’s realistic, so set one that you can stick to.

Here’s how to do it:

Compare your budget to your prior actual spending.

Any expenses that are cut should be limited to no more than a 20%-25% reduction based upon your prior spending.

For example, if you’re used to spending $1,200 per month on food, don’t try to drop down to $500. Start with lowering it to $1,000.

There will also be things that are layups, like canceling unused streaming services or getting rid of extra charges on your cell phone bill.

Aim for progress, not perfection. Give this first go-round a try and see where you end up.

How will you stay on track?

The keystone habit is your budget review, but it also doesn’t have to be super complicated or take a bunch of time.

The key habit to get your finances in order over the long term is tracking your spending.

It doesn’t have to take a ton of time.

I use my Five Minute Weekly Spending Review.

This method will help you focus on the key information without putting in more effort than you need to.

When you do a weekly budget review instead of monthly, you have four opportunities to adjust so you end the month on target with your goals.

Simply review your transactions over the last seven days, two to three key budget categories where you want to cut spending, and look at your overall net income month-to-date.

Set weekly spending targets for your overall spending based upon when your major expenses happen.

It’s the easiest thing to do that will have the greatest impact on budgeting. Get it on your schedule for the same time each week.

Budget Review Questions

After a month, it’s time for a budget review to see how aligned your expenses are with the plan.

Where was my budget successful?

The first time you budget, it won’t be perfect, but it will have some highlights and successes.

Review your spending at the end of the month.

Did you spend less in the areas you wanted to?

Was your overall spending down?

Focus on what good happened due to budgeting.

Where do you need to improve your budget?

You’re not going to hit every mark, but use it as motivation to improve. So what happened?

Were you too ambitious?

What came up that took you off track? Is it something that you could have anticipated?

Did you have some unexpected expenses like car repairs or unforseen housing expenses?

Things won’t be perfect, so look at what went wrong as information you need to get even better next time.

What progress did you make toward your goals?

Let’s keep this budget review positive!

How much money did you save? How much went toward investing or retirement contributions? How much debt did you pay off?

Even if you spent more than you made, did you close the gap compared to last month? That’s progress!

Remember, simply doing this budget review is progress toward your goals! Keep up the great work!

What budgeting changes will you make?

Every budget review will inform you of changes you need to make.

Remember, it doesn’t always have to mean cutting back.

Sometimes you can increase the cost of a budget category if you want to do more here.

Maybe you cut costs too much and increasing your budget is more realistic.

Maybe you realize food is ending up in the trash and want to reduce your groceries.

You don’t have to reach your ideal budget. Take it slow. It’s a gradual process, and the budget review will help.

Remember to schedule it!

Budgeting FAQs

Here are some of the more common questions I get when people are setting up their budget.

How many budget categories should I have?

I have one request: keep it simple to start.

Unless you’re a super spreadsheet person and you’re going to be doing a deep dive analysis on a regular basis, using the general categories is good enough.

Car insurance and home insurance aren’t going to change much, so forget about making a separate budget category for each one. Same with utility bills. Just lump it in as “auto” or “housing cost” for ease.

How do I budget for one-time expenses?

One-time expenses are more common than you think.

So you have to ask if it’s really a one-time purchase or if something like this can up again.

For example, vacations, holidays, etc.. aren’t really one-time; they’re actually irregular expenses.

At the end of the day, it’s an expense flowing out of your bank account, so it has to be accounted for with your finances.

Create a cushion in your budget and have an emergency fund to make sure you have room when they come up.

What if my income fluctuates?

Anyone who gets a year-end bonus would be considered as having a fluctuating income, but some have more wild swings.

We tend to ride the rollercoaster of spending more during our better income months and get into cost-cutting mode during the lean months.

But it would be better to set up an account to put money in during the high-income months and draw from during the low ones.

Open a separate account where your irregular income flows in (kind of like a business) and transfer out a “steady” paycheck to your regular bank account.

The more unpredictable the income, the more critical it is to create an emergency fund.

For more tips on managing an irregular income, you can check out another article I wrote on it right here.

Which budgeting system works best?

The system that works best is the one that will work for you, but here are some traditional (but in my opinion limited) methods to budget before I share my thoughts.

Some like the 50/30/20 budget (or sometimes referred to as 50 20 30 budget) where you spend 50% on fixed expenses, 30% on discretionary, and 20% toward your savings goals.

Others like the zero-based budget where you give every dollar a job.

The envelope system is getting harder and harder to execute as cash becomes less prevalent. People say it really works, but they weren’t able to sustain it over the long haul.

The fallacy is that it assumes nothing will ever come up that you haven’t budgeted for.

I have yet to meet a person who has that foresight.

Here’s where I’d start.

- Lay out your fixed expenses that would be a challenge to change (e.g. mortgage)

- Then your non-negotiable flexible expenses, the things that are most important to you.

- Earmark the rest to fund your savings goals.

This is a bit backwards compared to the “pay yourself first” thinking, but it tends to work better for many people.

Once you get a realistic budget, then you can flip it to save what you can first.

Remember, the best budget is the one that WORKS and you can COMMIT to.

Create the ideal budget given where you are today. Then review your past spending habits and reflect how to get from current to ideal.

What happens if I go over budget?

If you go a little over, don’t blow it all up completely.

It’s kind of like having a cookie when you’re trying to eat totally clean, then saying, “Well, I ate one, so I might as well just go for it!” Then you eat a half-dozen.

Give yourself some grace, and use it as information for the next time.

If you feel like a failure or give up until the budget resets, that’s a sign that your budget is too restrictive and that you are being too hard on yourself.

Instead of being critical of yourself, pretend you’re a supportive friend, then try again with this new information.

Should I just focus on making more money instead? Isn’t that easier?

Do everything you can to maximize your income, but don’t think it will solve your budget issues.

So many people I work with have a nice income but are spending right up to it. They wonder where their money is going and why they can’t save.

Making more money doesn’t always lead people to save money. Lifestyle creep happens

Spending tends to go up in lockstep with raises unless the budget issue is addressed.

Start first with tracking your spending and seeing what sustainable spending cuts you can make.

Then use my 50/50 Rule to save more (and spend more) as you make more.

Over time, you’ll see your savings rate climb and also you’ll enjoy having more money to spend on the things you care about.

Need help with these budgeting questions?

Spending is the #1 thing that will determine your future financial success. It is also a main source of conflict in relationships.

If you have budgeting questions or need help putting together one that will work for you over time, I’m here to help!

Schedule a free 30-minute call with me so we can talk through it.

For informational and educational purposes only. Information was previously posted by Rob Bertman, Family Budget Services, formally Family Budget Expert, prior to Mr. Bertman joining Focus Partners. The opinions expressed may not accurately reflect those of Focus Partners.