Lifestyle Creep: Don’t avoid it – Enjoy it AND build wealth even if you’re living paycheck-to-paycheck right now.

50/50 Rule Explained

We often feel like we have to choose between enjoying that hard-earned raise or bonus vs choosing to save or pay off debt with it. Lifestyle creep becomes the default and can get us into trouble.

Wanna know a secret? You can do both at the same time…responsibly.

Yes, lifestyle inflation can get out of hand in a hurry, but you don’t have to avoid it altogether.

That’s what The 50/50 Rule is all about. I’ll share with you what it is, why it’s important, and how it will impact your long-term wealth.

Table of Contents

What does lifestyle creep mean?

Simply put, it’s when someone spends more money as they make more money. When they increase their standard of living when as their income increases. Some call it lifestyle inflation too.

It’s the reason a couple who has grown their income from $60,000 a year to $250,000 is still living paycheck-to-paycheck, and even perhaps beyond their means.

Lifestyle Creep Examples

We’ve all done this before. We get a raise and start thinking about buying a new car or doing some work on our house. Perhaps we start to feel a little cramped and want to buy a new house with more space.

It’s kind of like going to the grocery store hungry. Everything you see looks good.

Here are some examples of lifestyle creep. It’s a list of the fun stuff many of us want to do:

- Upgrading your car

- Buying a bigger house

- Dining out more often

- Staying in nicer hotels on vacation

- Making major purchases when expecting a baby

- Getting the kids more expensive toys and electronics

- Impulse buying

None of these signs of lifestyle creep are bad on the surface, but the mindset shift can be dangerous.

Ever say to yourself, “I just don’t know where all of our money is going,” or “I feel like we do a pretty good job but we still can’t seem to save more money at the end of the month.” That’s how you know lifestyle inflation has gotten the better of you.

It’s natural to get a little more lax as we earn more money. We stop comparison shopping. We don’t feel like we have to track our spending. Major spending decisions are made on impulse rather than having to think about whether we can afford it.

We start thinking we have money to spend when we actually don’t. Remember that first job out of college when we used to stretch every dollar? This is quite different.

Dangers of Lifestyle Creep – Like a cup of coffee

Lifestyle creep is like a hot cup of coffee.

Coffee is your spending. Income is the size of the cup. Life is walking around your house with it in your hands.

The danger of lifestyle creep is the risk of spilling the coffee and burning yourself (let alone WASTING COFFEE!).

If the hot cup of coffee is filled to the brim (aka spending all that you make), you might not realize the danger. You might even think, “This is great! I have a full cup of coffee!”

Then you get a bigger cup (make more money) from work or your kids make you one for your birthday, but you want more coffee too so you fill it up to the brim (spend more money).

But when life gives you something unforeseen (like stepping on a lego on the floor), it can cause a serious spill, a painful burn on your hands, and maybe even a dropped and shattered mug.

That’s the danger of lifestyle creep.

If life throws any challenge your way (a major unexpected expense or a loss of income) it causes a giant financial mess and stress because you can no longer pay all of your bills and you don’t have the savings as a backstop.

Should you avoid lifestyle creep?

Heck no! You should absolutely be able to spend more money as you make more.

BUT…It can’t come at the expense of sabotaging your financial freedom and your financial independence.

We need to manage lifestyle creep by balancing our lifestyle upgrades with sound financial decisions.

If we spend every extra dollar that we make and focus on payments we can afford rather than taking a balanced approach, it can put us in some serious financial peril.

There’s a responsible way to enjoy lifestyle inflation while building wealth at the same time.

Enter The 50/50 Rule.

What is The 50/50 Rule?

It’s the responsible way to both spend more money and save more money over time. It works no matter if you’re living paycheck to paycheck right now, saving 10% of your income, or if you’re using the 50-30-20 budget.

The formula is simple. Any extra income you get, take 50% of it and add it to what you’re currently putting toward saving, investing or paying off debt. Take the other 50%, and feel free to spend it guilt-free.

Let’s say you get a nice $6,000 pay raise. That’s $500 per month.

Using the 50/50 Rule, you’d add $250 each month to your current savings. Take the other $250 and feel free to spend it. In the end, you’d be saving $3,000 more per year and spending $3,000 more per year.

How is The 50/50 Rule different than what others do when they make more money?

Most people take lifestyle creep to the extreme and spend every last penny of that awesome raise or bonus (and often more). Some keep a constant savings rate (like 10%) even as they make more money. But you can do better than that all of them.

If we were to look back at our first job out of college when we were making next to nothing (I was making $26,000 living in Chicago), and look at what we’re making today, how are we not saving more each month and why don’t we have more money saved?

Well if you’re like many people, you’d take a $6,000 pay raise and spend all of it before it even hits the checking account. In fact, some even spend more than the increase in income (eg. buy a new car for $600 per month or spend $10,000 on home improvement), putting them further in debt. That’s lifestyle creep at its worst.

But let’s say someone is responsibly saving 10% of their income, they’d still have a $450 per month increase in spending and only save $50 extra per month. That stagnant 10% savings rate isn’t enough to reach financial independence.

The 50/50 Rule will make sure you’re taking half of every extra dollar earned to go towards building your wealth. It also allows you to spend more money guilt-free without going overboard.

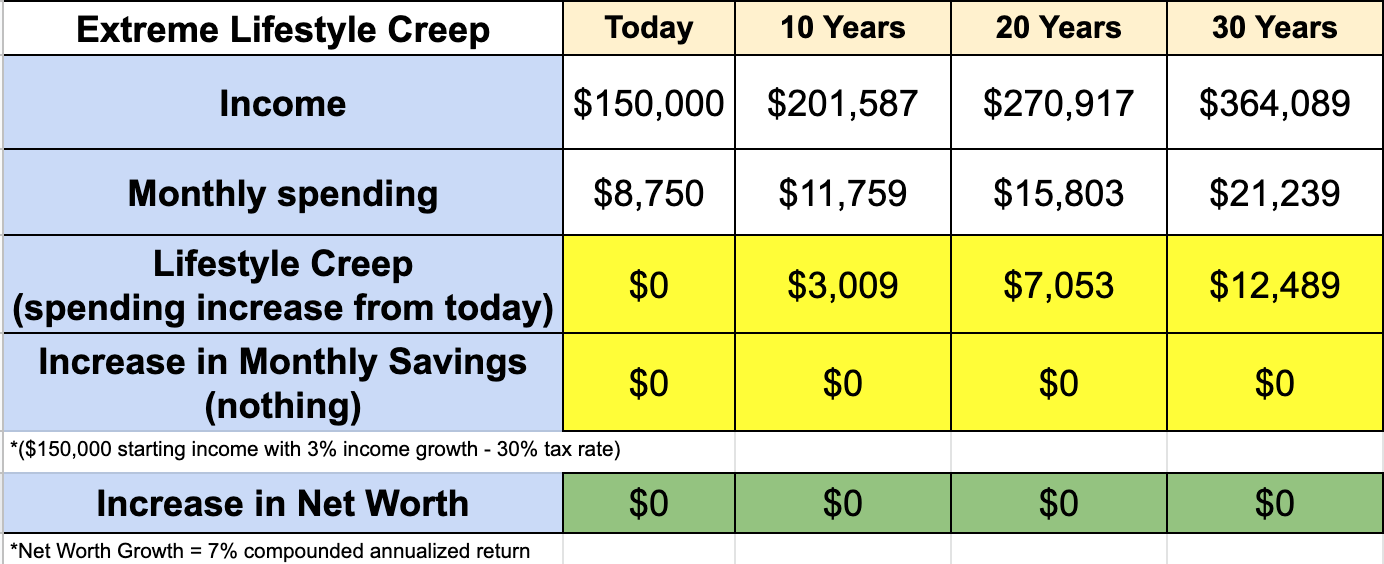

Extreme Lifestyle Creep vs Lifestyle Inflation with The 50/50 Rule

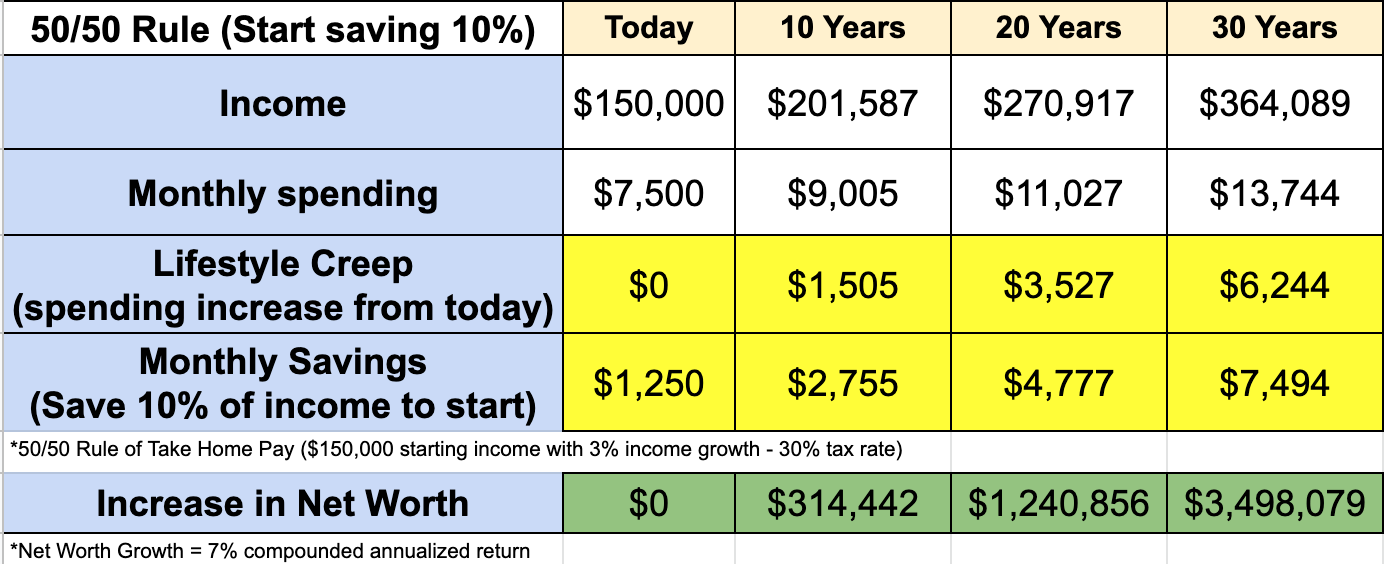

Let’s look at Mike & Brittney. They earn $150,000 together and have steady careers with 3% projected income growth over time. They don’t have any money in a savings account at the moment, but they hope to get there.

In this first scenario, let’s assume they have extreme lifestyle creep and spend every extra dollar they bring home over the years.

What does lifestyle creep at its worst look like? Well, actually the day-to-day actually looks pretty good. Spending every dollar of take home pay allows for a very nice lifestyle.

But the downside can be very treacherous, because lifestyle is built like a house of cards. Any hiccup in income (like many experienced with COVID-19) or any major expense means that the house comes a-tumblin down. The wheels fall off.

Plus, there is absolutely no way that they can ever stop working. It’s either that or live off of social security and live on dimes compared to what they’re used to.

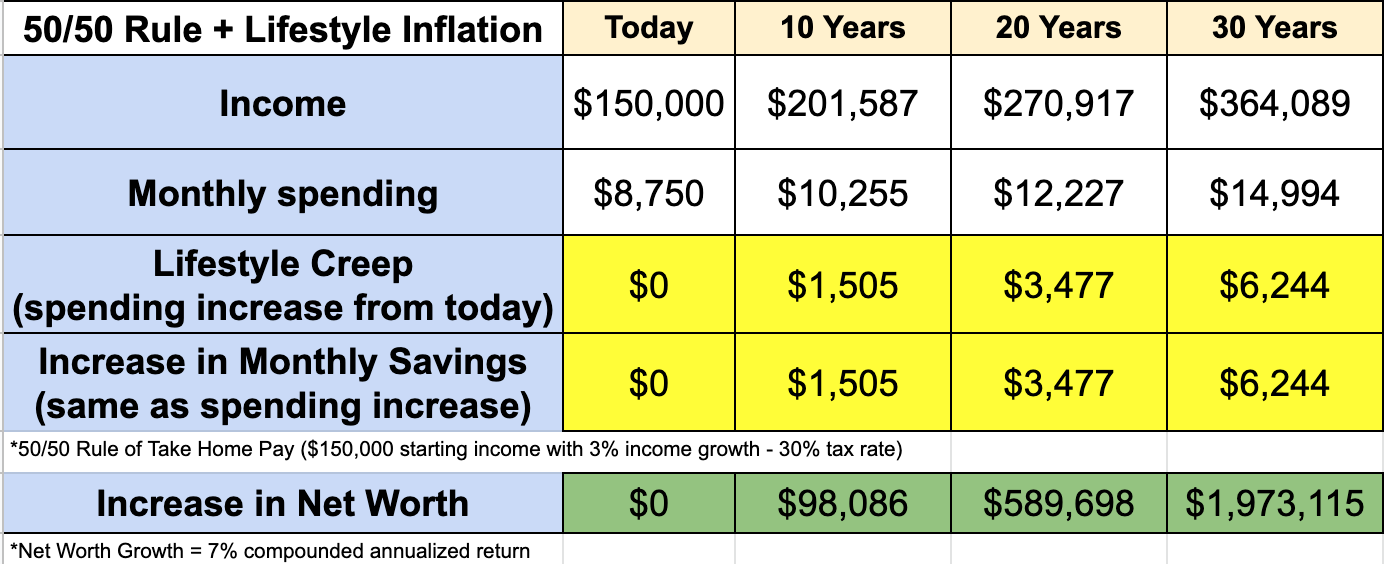

Brittney & Mike make the wise choice to commit, at minimum, to using The 50/50 Rule with some lifestyle inflation. It gives the best of both. Their lifestyle can grow in lock step with the amount of money they save each month.

See, The 50/50 Rule can build wealth significantly even in a career path with steady growth. They’ll end up with an extra $2,000,000 after 30 years while still spending more money along the way.

It’s a great balance between enjoying those hard-earned raises and also being financially responsible with it.

How does The 50/50 Rule apply to bonuses, tax refunds, and expenses/debt payments?

The 50/50 Rule applies to many other areas where more money comes into your life for one reason or another aside from regular salary raises.

Tax refund: Got a $5,000 tax refund? Spend $2,500 of it as long as you’re taking the other $2,500 to build your wealth.

Bonus: Get a $10,000 bonus? Take either $5,000 of it or 50% of your take home pay toward wealth builiding and feel free to spend the rest.

Daycare expense: One of your kids getting off the daycare payroll and headed to Kindergarten? Take half of what you were spending and keep spending it. Take the other half and add it to what you’re saving, investing or paying back debt.

Credit card debt & Past due bills (This one is different): Credit cards & past due bills should be wiped out as fast as possible so The 50/50 Rule doesn’t apply here. After paying off one put 100% of that past payment toward the next credit card or past due bill until all of them are eliminated.

Other debt payments: The 50/50 Rule can apply here after paying off student debt, an auto loan, or a home equity loan. Feel free to keep half of the former payment going to build your wealth. However, if you feel behind, take 100% and pay off more debt or increase the money going toward your savings/investments.

Large inheritances or gifts: If you’re in the fortunate position to receive a major financial gift from a relative, hold off on The 50/50 Rule until you talk to a financial professional. Depending on your financial situation and the size of the money received, it’s possible that you may want to put more than 50% toward building your wealth, a lot more.

As you can see, The 50/50 Rule applies to any money that comes into your life. 50% to build your net worth is just the minimum amount.

If you want to accelerate toward your goals, then feel free to spend less than 50% and put the rest toward things that will push you along at a faster pace.

Save more money today, then apply The 50/50 Rule to explode your wealth

The whole point of The 50/50 Rule is that you can build a nice nest egg even if you’re having trouble finding ways to save more today. Plus, you don’t have to avoid lifestyle inflation. You can enjoy it!

But…

What if you could find more money today to pay off debt, save, and invest, THEN apply The 50/50 Rule.

Let me make this fairly simple. Every extra $1,000 per month that a family has left over, can turn into some major money. Here’s a chart of how putting an extra $1,000 each month to either pay off debt or invest can increase your net worth over time:

In other words, every extra $1,000 per month you find today could mean $1,000,000 in 30 years.

Here’s what it could look like for Brittney & Mike if they save 10% of their income today then apply The 50/50 Rule for all increases in income:

Take a look at that increase in net worth. That 10% savings rate today means building their net worth by $200,000 more in 10 years, $600,000 more in 20 years, and $1,500,000 more in 30 years than using The 50/50 Rule on its own.

You can do it too, you know.

“That sounds great Rob, but I don’t know where to start? We’ve tried budgeting, and it hasn’t worked for us. Plus we can’t seem to stop arguing about money.”

I’ve seen just about every relationship dynamic you can think of so you’re not alone if you’re struggling with lifestyle creep of your household budget. But I can tell you that it is possible to save 10% of your income even if kids are breaking the bank or you don’t get along with money.

This is where I can really help out.

Get Budget Help to Save More Money Today

The Family Budget Transformation System is the fastest way to go from feeling stuck and stressed about money to dramatically improving your financial future and relationship.

The average client I’ve worked with has cut their spending by 18%. That means that even if someone has been overspending and going into credit card debt, they could reverse it and get to a 10% savings rate. Couples who have been living paycheck-to-paycheck despite earning a six-figure income boost into a double digit savings rate as well.

*This works even if you’ve already cut your spending due to the pandemic. In fact, two couples started working with me recently because income is down and they know there’s more they can do to spend less.

Not only will we figure out how to find that extra money, but we’ll cover what you should do with it (save, pay off debt, or invest).

Imagine being able to stop stressing about money and arguing with each other to feel confident that your personal finances are on the right track and you’re finally working together to get there.

If all you did was stay where you are and apply The 50/50 Rule, you’d be 2-4x better off than you are today. But if you’re ready to jumpstart your way to financial independence and a relationship free of money fights, I’d love to learn about where you’re struggling and see if I’m a fit to help out.

This is what I do, because it transforms families’ financial futures as well as their relationships.

I’m here to help!

Not ready to talk, but want budget help?

For informational and educational purposes only. Information was previously posted by Rob Bertman, Family Budget Services, formally Family Budget Expert, prior to Mr. Bertman joining Focus Partners. The opinions expressed may not accurately reflect those of Focus Partners.