If you’re reading this, chances are you fit into one of these three categories:

- You own a house and feel financially stretched.

- You took on a home improvement project that cost you more than you expected.

- You are actively looking to buy a house of your own but prices have gone up so much you’re wondering how much house you can afford.

This has pushed housing prices up all over the country as well as the cost of home improvement projects.

The combination of higher prices, house fever, and the fact that housing costs are one of the largest budget categories means that it’s really easy to end up house poor.

You’ve at least thought about changing your housing situation in some way due to the pandemic & historically low mortgage interest rates.

This one decision can make or break your financial situation (and can even ruin your relationship too) so let’s take a look at how we can avoid being house poor and how to get out of it if you’re there right now.

Table of Contents

What is house poor?

Being house poor means that the total cost of homeownership leaves little room for discretionary expenses and makes it hard to fund your financial goals. You may also know it as “house rich, cash poor”.

It’s hard to live below your means if your housing costs are too high.

The conventional rule of thumb for house poor is the 28%/36% rule. Keep your housing costs under 28% of gross income and all of your debt payments including your mortgage under 36% of gross income.

Let me be clear. I disagree with these rules of thumb.

They don’t account for the other pieces of your life and using them leads to mistakes when buying a home.

Mistakes that lead to being house poor

Buying a house is one of the biggest financial decisions people will make. Yet, it always amazes me that people put so little thought and effort into it.

Don’t get me wrong, people seek out information before buying a home.

It just so happens that it’s usually from people who have an incentive to have you spend as much as you can rather than getting you into a house you can comfortably afford.

Avoid these major mistakes that lead to being house poor:

Underestimating the cost of homeownership

When I work with my clients who are looking to buy a house, the banks are really good at telling them the principal and interest portion of the payment.

Some assume they can afford a mortgage equal to their current rent payment, but that’s a recipe to become house poor.

The monthly expenses of owning a house go way beyond that.

Costs of home ownership include:

- Principal and interest payments

- Property taxes

- Homeowners Insurance

- Maintenance and upkeep

- Utilities

- Home improvement projects

- Furnishings

- Landscaping and lawn care

That doesn’t even include homeowners association (HOA) or condo fees. Nor does it include mortgage insurance (PMI) if you don’t put 20% down on a home.

Create a household budget that includes the entire cost of homeownership and not just the mortgage payment to avoid this mistake.

Trusting the bank to tell you how much house you can afford

When you think of borrowing money from a bank, you probably think of having to have a pristine credit report and clean finances.

But with mortgages, it’s much easier to qualify.

Banks use a flawed metric (IMO) called the debt-to-income ratio (DTI). This metric adds up your debt payments and divides it by your gross income. Lenders will allow a 43% DTI!

A few things baffle me here about the debt-to-income ratio that banks use:

- The calculation is based upon gross income and not take home pay. That means a bank could be ok with 60%+ of your take home pay going to debt! Talk about being house poor!

- The debt calculation is based upon your monthly payments, not how much debt you owe. This incentivizes borrowers to pay off loans as slowly as possible. Someone with $120,000 of debt and paying $2,000 per month has a worse chance of qualify than if they refinance to a longer term loan to lower their monthly payments to $800. But they still have the same amount of debt! Most credit cards only require the minimum payment to be 2% of the outstanding balance which doesn’t make a dent in the principal for cards with 20%+ interest rates.

- DTI looks at your projected housing payment going to principal, interest, taxes & insurance (PITI) and HOA fees if applicable. But the homebuyer needs to know that there will be other costs for maintenance and utilities that go along with owning the home. That can be 1-3% of the cost of the house and needs to be in the housing budget.

Guessing how much money you spend each month

I used to make this mistake, and I’ve seen many others make it too.

Being a numbers person, I thought I knew how much I was spending each month without really tracking it. But I was very wrong until I started looking at the actual numbers. I wasn’t alone.

When I start working with my clients, I ask them to give me a ballpark of what they’re spending each month before we look at the actual numbers. In every single instance, the actual number is much higher than the estimate. It’s at least $1,000 per month off and often it’s $2,000 or more.

People who guess their monthly spending (instead of knowing the actual number) can end up house poor because the mortgage payment may cause them to overspend each month.

Forgetting about the other things you want to do in life

If your house is your sanctuary, then by all means, feel free to take a larger part of your income to put towards your house.

But if you have other things you’d like to do that help you enjoy life and feel more fulfilled including travel, date nights, spending money on your kids’ activities, or driving a certain car, then spending more on a house will leave little room for those other things.

What about financial goals? Do you want to save for retirement or kids’ college? Pay off other debt? Become financially independent? Start a business? Spending more on a house means less money to put towards those things too.

Thinking that all you need is money for the down payment

There’s a lot more money needed to buy a house outside of the down payment, maybe even 5-10% of the cost of buying a home.

Why would you need that much money? There are two major reasons.

The closing costs on a house surprised many of my readers.

It can be anywhere between 2-5% of the purchase price between the loan origination fee, funding the escrow account, title fees and title insurance, prepaid interest, potential upfront mortgage insurance, etc.

Aside from closing costs, I have yet to meet the family who just moved into a new home without spending a dime on anything else. See more on family budgeting.

Chances are you’ll want to buy new furniture, decorate, get a new TV (or TVs), paint, put in new floors, redo the kitchen or a bathroom, and on and on.

Not only do you need money for all of that, but you also need to have an emergency fund AFTER the down payment and the other expenses because something else will come up.

Families who save money only for the down payment may end up putting less money down.

This leads to a higher monthly mortgage, and the desire to pull money out of investments and retirement accounts to buy the house, cover the closing costs, and take on the other home projects.

That’s a really good way to take a step back on your financial goals and become house poor.

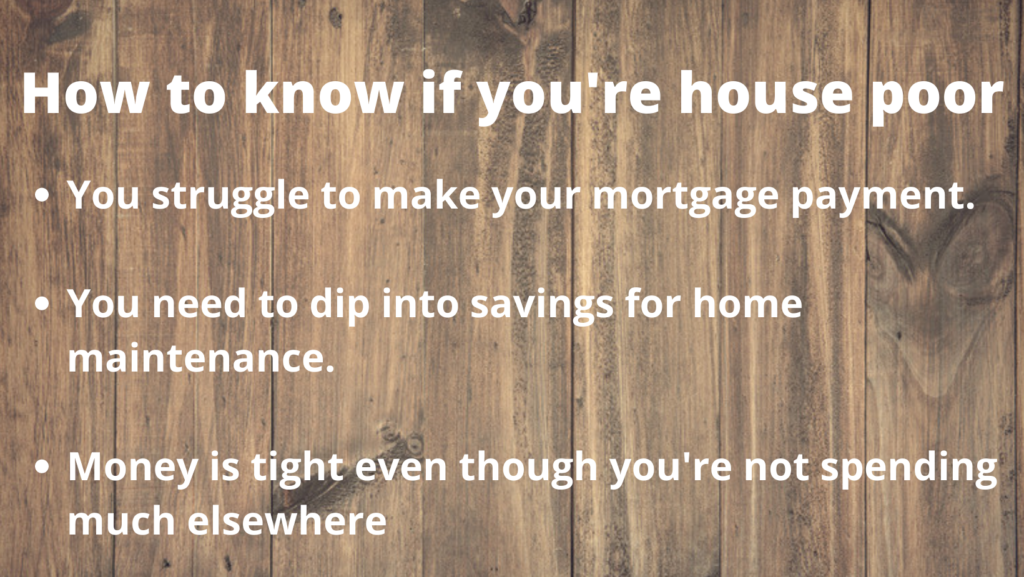

How to know if you’re house poor

Here are signs you might be house poor and spending too much of your income on housing expenses:

- It’s a struggle to make your monthly mortgage payment each month.

- You have to dip into your savings for home maintenance.

- Money is tight even though you aren’t spending much money elsewhere.

- Owning your house is much more expensive than you thought it would be.

- You think to yourself, “I wish we would have spent less on this house.”

These signs are not really about the numbers.

They are about the stress that comes with the high costs of owning your house and the things it stops you from doing because you don’t have the money.

If you feel like you’re house poor, I have some ideas on how you can get out of that stressful situation.

How can I stop being house poor?

When you’re house poor, you have to find money from other areas to stop living paycheck-to-paycheck or even spending more than you make on a regular basis.

This extra money can come from big chunks or from cutting back on the day-to-day spending.

Here are some examples of what to do if you’re house poor.

Big changes

- Make more money

- Get a second job or a side hustle

- Ask for a raise or work more hours

- Change your housing situation

- Downsize to a more affordable home

- Sell your home and rent instead

- Find someone to move in and pay rent

- Refinance your mortgage to extend the term and lower your payment.

- Sell your car or trade down in car

- Send the kids to public school instead of private school (if applicable).

Cut back on small things that add up

- Track your spending and review the areas where you can cut back.

- Limit discretionary spending

- Cancel some streaming services.

- Cook at home more.

- Use savings to pay off other debt to eliminate those monthly payments

- Sell things you don’t need on Facebook Marketplace or Craigslist

- See what you can sell on Decluttr.

- Cancel your vacation and book a less expensive one.

- Spend less money on clothes.

Here’s a post I wrote on other tips to stop spending money. I share other ideas to reduce your expenses without having to change your lifestyle.

(If you need help with this, schedule a 30 minute discovery session with me, so we can talk through it.)

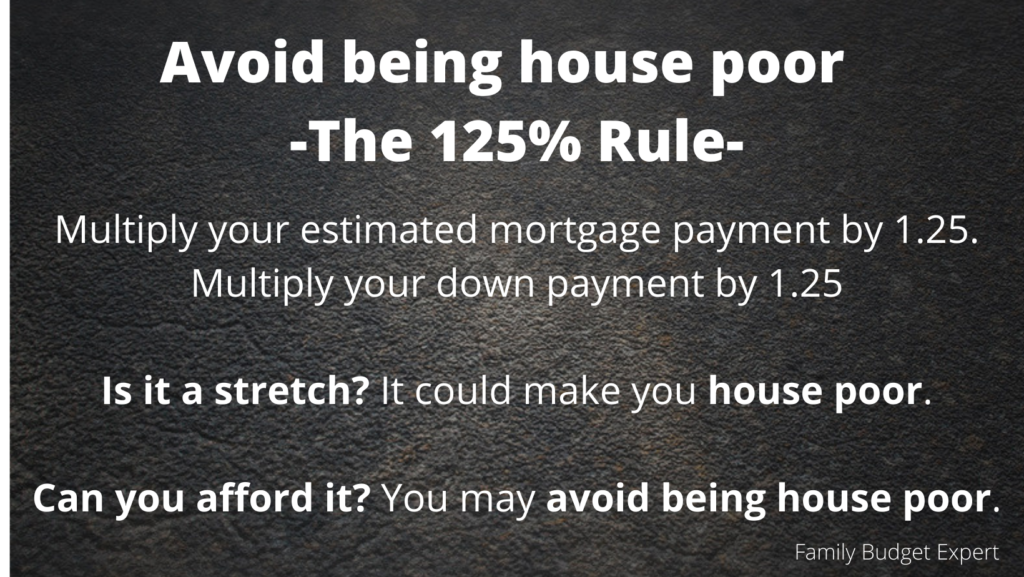

How to avoid being house poor – The 125% Rule

Let’s say your housing situation is fine right now, but you’re looking to buy a bigger house or go from renting to owning.

The best way to avoid being house poor is by using my 125% Rule.

This rule is your sanity check to have a higher probability of affording the house you buy. It will make sure that you have a big enough cash cushion to account for the true cost of owning a home.

Here’s how my 125% Rule works for both the monthly payment and the down payment.

If the monthly mortgage payment you are looking at is $2,000 per month, make sure you can afford $2,500 ($2,000 x 125%). If that’s a stretch, then any extra maintenance or upkeep will make you house poor.

If you need $60,000 for your down payment, plan to save at least $75,000 (125% of $60,000). That way, you’ll have extra money to put into the house, to furnish it, and to cover closing costs.

The 125% Rule is the minimum you should shoot for.

Why does this rule work?

Well, the reason people become house poor is because they have too much money going toward housing expenses. The 125% Rule will make sure you have enough money to cover the other expenses of owning a house outside of the mortgage and down payment.

Other experts say the ways to avoid being house poor include:

- Buy a starter home

- Be debt-free before buying a house

- Make a larger down payment

- Cap the home purchase price to 2-3x your income

- Set up a housing emergency fund

- Stay below a DTI of 28%

The 125% Rule is the simplest way to avoid being house poor because all it takes is one simple calculation.

But there are other great ways to avoid being house poor that doesn’t dive into the numbers:

- Talk to trusted friends and family who have been homeowners for a while. What do they say about it? What have they seen that you didn’t think of?

- Ask yourself why you want to own a home instead of renting. Don’t rely on the “rent is throwing money away” thing, because rent won’t wreck your finances like homeownership could.

- Is the extra space of a bigger home worth giving up other life experiences and long term goals?

- Think of your contingency plan if you become house poor. What will you be willing to do if you have to free up other money outside of raiding your retirement or going into more debt?

Yes, crunch the numbers, but also talk to people who own and go over these questions with your spouse.

Not sure how much house you can afford or feel stuck with the one you own?

There are plenty of ways to make sure that the real estate you own doesn’t destroy your personal finances.

Your house or condo will be one of the most expensive things you’ll ever buy, so approach it as if you were looking for a new job or making a career change.

Do your research and due diligence. Actually crunch the numbers, talk to experts who don’t have any financial incentive in the decision you make, and ask yourself what you’re really looking to get out of it.

Whether you feel like you’re house poor now or want to make sure you avoid it, you can make it happen!

I’m here to support you however I can.

If you are:

- Looking to see how much house you can truly afford, or;

- Feeling house poor and need help getting out

Set up a free discovery session with me. We’ll talk through it and see how to make it happen.

Need help cutting your spending but not ready to talk?

Check out my free guide: 5 Steps to Cut Spending so you can FINALLY pay off debt

For informational and educational purposes only. Information was previously posted by Rob Bertman, Family Budget Services, formally Family Budget Expert, prior to Mr. Bertman joining Focus Partners. The opinions expressed may not accurately reflect those of Focus Partners.