December 3, 2025 How to Make a Realistic Holiday Budget for Families (Without Overspending or Feeling Guilty) by Rob Bertman, CFA, CSLP®, CFP® in Budgeting Read

October 22, 2025 How to Create a Family Budget that Actually Works (While Keeping The Lifestyle You Love) by Rob Bertman, CFA, CSLP®, CFP® in Budgeting Read

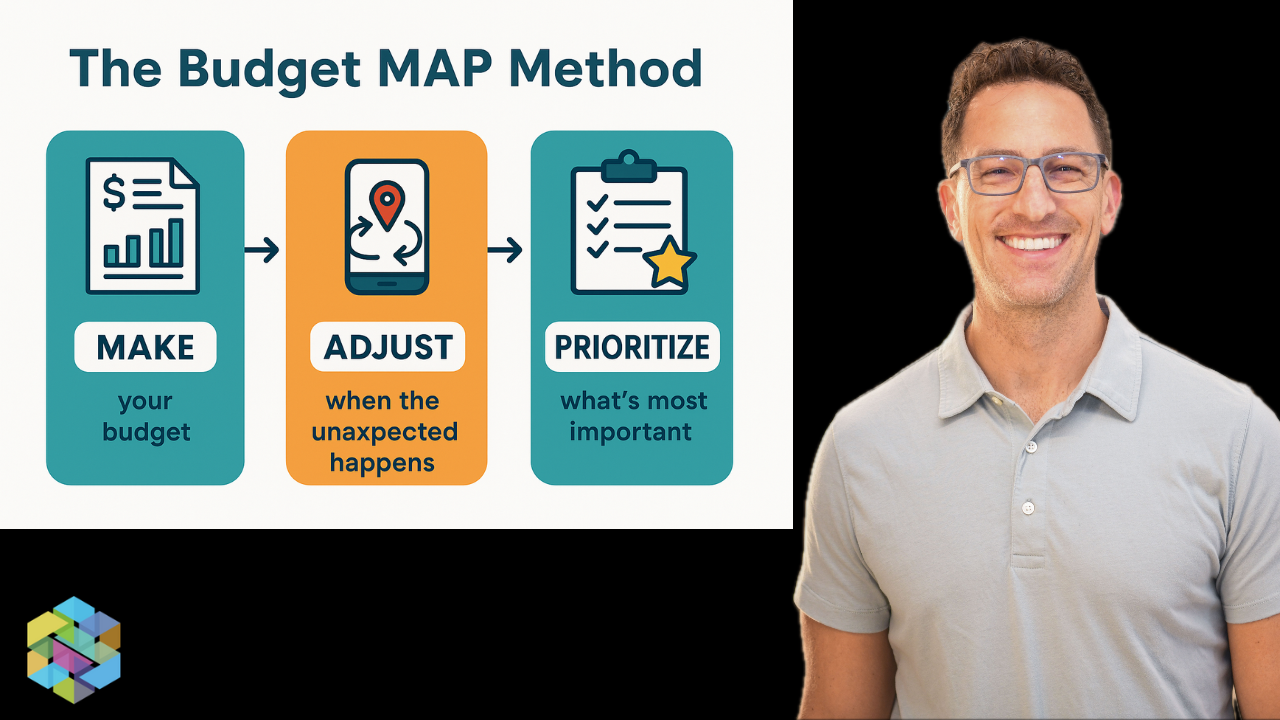

July 23, 2025 The 7 Most Popular Budgeting Methods for Busy Families (and How to Choose The Right One for You). by Rob Bertman, CFA, CSLP®, CFP® in Budgeting, Most popular blog posts, Spending Read

October 8, 2024 What Is a Sinking Fund and Why Is It Important in Budgeting? by Rob Bertman, CFA, CSLP®, CFP® in Budgeting Read

September 30, 2024 Separating Business and Personal Finances by Rob Bertman, CFA, CSLP®, CFP® in Budgeting Read

September 27, 2024 10 Key Components of Successful Budgeting by Rob Bertman, CFA, CSLP®, CFP® in Budgeting Read

September 5, 2024 Weekly Budget: Give it a try with these 5 simple steps. by Rob Bertman, CFA, CSLP®, CFP® in Budgeting Read

August 26, 2024 Budget Categories: Long list or short list? by Rob Bertman, CFA, CSLP®, CFP® in Budgeting, Most popular blog posts Read

April 17, 2024 How to spend less money:10 tips WITHOUT drastically changing your lifestyle by Rob Bertman, CFA, CSLP®, CFP® in Budgeting Read

April 6, 2024 10 Budgeting Questions: How to Spend Less While Enjoying Life by Rob Bertman, CFA, CSLP®, CFP® in Budgeting Read