Irregular income: How do you successfully budget with it?

Are you self-employed? Working on commission? Participating in the gig economy?

You most likely have an irregular income that is a challenge to budget for.

Chances are that the lean months are too lean to support your expenses so you go through the cycle of going into credit card debt then paying it off later.

But boy are the good months good! You think, “If I didn’t have to dig myself out of a hole, I might actually build some wealth and reach my financial goals!”

This stressful cycle doesn’t have to be this way.

You can budget with an irregular income. All it takes is a tiny bit of planning to make it happen.

It includes figuring out how much your variable income fluctuates, going from behind to getting ahead then setting yourself up with a “steady paycheck”.

Table of Contents

What is an irregular income?

Living on an irregular income means that your monthly income is unpredictable and can fluctuate. There’s no steady paycheck or predictable income you can plan around.

Examples of irregular income include:

- Self-employment income

- Commissions based income

- Quarterly or annual bonuses

- Collecting tips in the service industry

- Part-time work with irregular hours

- Seasonal work (like landscaping or accounting)

- Stock options, stock purchase plans or restricted stock units (RSUs)

Budgeting with a variable income like this each month can be stressful.

Will this be a month I have to dip into savings or go into credit card debt, or is this a month where I’ll be able to finally catch up and maybe get ahead?

Let’s discuss how to break the cycle and smooth our irregular income.

How to budget with an irregular income in 10 steps

Now it’s time to go from being behind to getting ahead. A little bit of planning will go a long way to solving the problem.

Take the steps to do this and it can save you a year of financial stress.

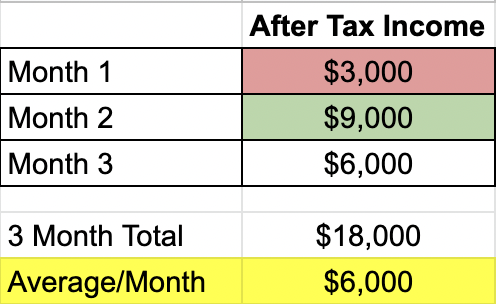

Step 1: What is your average monthly income?

Pull up your income history for up to 12 months. If you can’t go back that far, just go with the last 3 months. More is better though.

Plot it out on a piece of paper or spreadsheet and note the following numbers:

- Highest monthly income

- Lowest monthly income

- Average monthly income

What’s the difference between the highest and lowest? In other words, how lean is the leanest month and how flush is the highest month?

The closer the numbers are together, the easier it is to plan for it and there’s less risk for you.

If the numbers are drastically different (like close to double or more), then that’s a greater risk which requires a more conservative plan.

Here’s what the calculation could look like:

Step 2: Add in spousal income.

Now that you know your monthly average income, add in your spouse’s income too.

If they have a steady paycheck, it will be easy. Just plug it in.

If they have an irregular income like you, then repeat Step 1 to figure it out.

This is the average monthly household income, but there are some months where it would be lower and some months where it would be higher.

In this example, the low household income for the month was $8,000 and the high was $14,000.

Step 3: List your fixed monthly expenses and your flexible expenses.

It’s time to get your expenses in order and figure out how much you have going out on a monthly basis.

The fixed expenses are bills that you have each month like clockwork as well as putting food on the table.

Fixed expenses include:

- Mortgage payments / Rent

- Utilities (gas, electricity, water, trash)

- Car payment

- Groceries

- Phone / internet / wireless

- Home & auto insurance

- Health / medical

- Kids daycare / School tuition

- Other debt payments (student loans, credit cards, etc)

- Pet expenses

These are bills you must pay/stay current with so that you don’t run the risk of financial ruin.

Flexible spending includes:

- Dining out

- Travel

- Kids’ discretionary spending

- Clothing & accessories

- Hobbies

- Non-essential Amazon, Target & Walmart purchases

- Electronics & technology

- Home improvement

- House furnishings

These are the items that you normally spend money on but you have a say in how much from month to month.

If you’re not sure what you actually spend, you’re certainly not the only one!

I suggest signing up for a budgeting app like Mint.com. It will pull in the last 90 days of transactions so you can see your ACTUAL spending.

(Besides, the #1 habit you can do to improve your finances is to start tracking your spending – certainly before you can create a budget.)

Step 4: List your irregular expenses and add the average to your spending.

Expenses can be irregular too. They come up from month to month.

Lean months of income combined with birthdays, holidays, summer camp costs, etc can be really stressful.

If you notice that this happens to you, then you’ll want to make sure you’re aware of these expenses too.

Here’s an article I wrote on how to budget for irregular expenses. This goes hand in hand with planning for an irregular income.

Add that smoothed out monthly number into your fixed expense calculation.

Step 5: Add in your debt payments.

Total up how much you have going toward your debt each month outside of your mortgage and car payment.

We’re talking student loans, credit card debt, and other things on payment plans.

These debt payments need to be made but eventually, these will go away once they’re paid off.

Step 6: Figure out what your monthly paycheck should be.

Let’s say that the regular fixed and flexible expenses come out to $8,500 and you have another $500/mo in irregular expenses ($6,000 per year). Plus you have $1,000 going toward debt other than your mortgage or car payment.

That means your monthly expenses are $10,000.

Your spouse is bringing in a steady $5,000 per month and your average is $6,000

The goal here is to turn your variable income into more reliable regular income, so $5,000 per month will allow you to cover your expenses for the month.

That’s your paycheck.

Why not the full $6,000? That’s because we’re going to hold back some money to get you ahead.

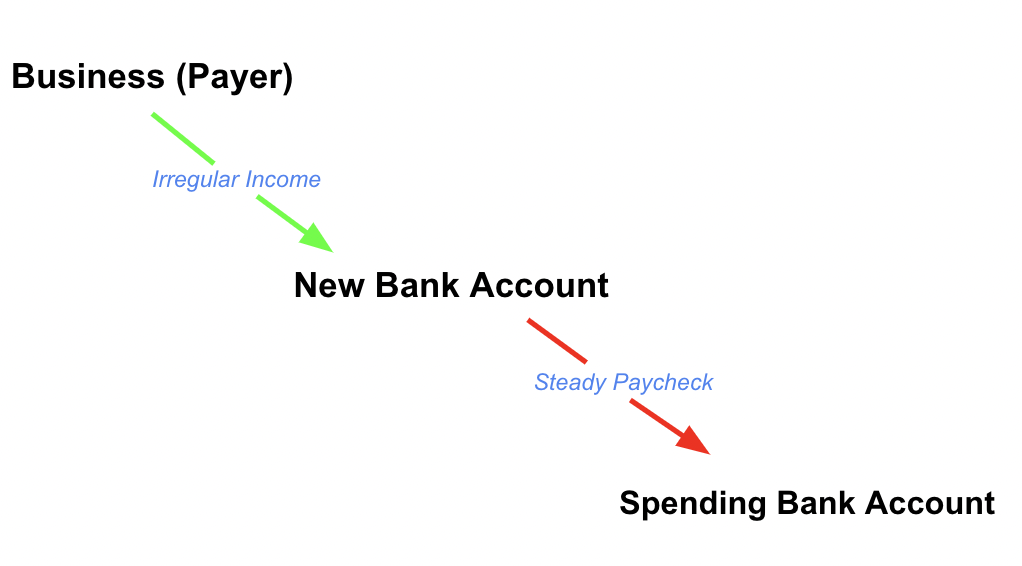

Step 7: Reconfigure your bank accounts.

In order to smooth out your fluctuating income, you’ll want to set up an intermediary checking account or savings account.

All of your variable income will flow into that account. Then you’ll set up an automatic transfer of your “steady paycheck” from that account into your normal personal account.

Step 8: Build a buffer.

You’ll want to build up a buffer in this new bank account so that even if you have a lean month, you can still transfer your “regular income”.

Think of this like an emergency fund of sorts.

Get started by building up a 3 month shortfall. Take your average monthly income (from step 1) and subtract your leanest month.

In the example above, the average is $6,000 per month with the leanest month being $3,000.

The buffer to build up and keep in there is $9,000. That’s 3 months times the $6,000 average minus $3,000 leanest month or

3 x ($6,000 – $3,000) = $9,000

Now you’re protected against a very lean season.

Step 9: Pay off your credit card debt.

The bedrock of a solid financial foundation is having an emergency fund and being credit card debt-free.

This is a real challenge for those with irregular income, but it should be a goal to pay off debt during the great months.

Think of the credit card debt as the hole you need to dig out of. The buffer from step 8 is filling the hole back up with dirt so you don’t fall back in.

Step 10: Free up extra money so you can accelerate your way toward financial stability.

We all spend money on things that don’t hold any value in our lives, and budgeting just doesn’t work for most people.

But if you can find the spending that doesn’t matter to you, you can save money even faster than before.

It is so critical to lean your spending because the amount of money you have leftover at the end of the month after your income and expenses is the bedrock of personal finance.

It’s the most predictive factor of financial success (not how much you make believe it or not).

Learn how to create a family budget that sticks using my Keep, Cut Back, Eliminate Method to free up extra cash on your terms while still doing the things you enjoy most. Family Budget Planner

What do I do with the extra cash?

It might take you a few months or even a year to get ahead after being behind.

After you reach the milestones of building that buffer and paying off credit card debt, it’s time to figure out what’s next.

Think of any extra cash in the buffer account like a bonus that you can payout quarterly.

That money should be split between increasing your lifestyle and building your wealth. Use my 50/50 Rule to balance lifestyle creep and reaching your financial goals.

Book a free consult to talk through this with me.

I’m here to help you any way I can, so I offer a complimentary 30-minute consultation with anyone who wants it.

We can talk through your challenges of irregular income, budget, or anything else that’s on your mind.

If you’re not ready to talk but want help with your budget,

For informational and educational purposes only. Information was previously posted by Rob Bertman, Family Budget Services, formally Family Budget Expert, prior to Mr. Bertman joining Focus Partners. The opinions expressed may not accurately reflect those of Focus Partners.