How to pay off your debt FASTER: Even if you have a lot of it.

If you have a ton of debt, you’re not alone.

In fact, US credit card debt just hit an all time high, and that doesn’t even include Buy Now, Pay Later stats.

Look, I’m not here to tell you that debt is bad and that you need to pay it off as fast as you can at all costs.

BUT, carrying debt is extremely stressful and can get in the way of otherwise thriving finances (and relationships).

So many people I talk to go through the cycle of paying off debt then getting back into debt.

“Something always seems to come up to put us right back into it,” is something I commonly hear.

It’s just hard to get ahead when you have so much of your monthly take home pay going to debt repayment.

There’s not a whole lot of wiggle room if something “unexpected” comes up.

Table of Contents

Why is paying off debt important?

There are 3 reasons why it’s important to pay off debt:

Paying interest makes a purchase more expensive.

Most people start with talking about the interest rates on debt. It is certainly a factor, but it’s NOT the most important.

Why are other things more important?

Well, many play the game of lowering the interest rate on their debt by taking out personal loans, consolidating, zero interest transfers, and…

It doesn’t solve the problem. The debt doesn’t get paid off any faster.

Does it help? Sure, but the cycle usually continues.

The reason I want to start here though is because it was probably the first thing that popped into your mind.

So the fact is that debt makes the cost of buying things more expensive because you have to pay back what you owe plus interest.

The amount of money you have to shell out to pay off debt is more than the actual cost if you had paid for it in cash.

Many families carry high interest credit card debt which can be the hardest mountain to climb.

We all know this, so now let’s move on to the next two factors which are more important in my mind.

Debt payments eat up your monthly cash flow.

When families see how much is going to debt payments each month, it really solidifies their motivation to become debt free..

Things feel tight each month because not only do they have to keep up with the day-to-day ongoing expenses, but they also have to pay off debt at the same time.

It’s like trying to fill up the bathtub with the drain wide open.

It’s like trying to complete that important project due tomorrow while trying to finish the one that should have been done last week.

It’s hard to get ahead when you’re always playing catch up, and that’s what debt is.

Debt is money you’ve already spent but haven’t paid for yet.

Yes, the interest rate is important, but freeing up cash flow and lowering monthly expenses makes the family finances much more stable.

(Need help finding extra money in your budget?)

It’s the most common source of money fights

You always hear that money fights are the #1 cause of relationship and marriage problems, but let’s get more specific here.

Seriously, how many times have you argued about your allocation in your investment portfolio or the amount of term insurance you have. I have NEVER seen arguments about these.

The real cause of money arguments is spending and debt. It’s a real point of stress with the couples I work with.

To take it a step further, I have worked with plenty of families with a really solid net worth, but they have consumer debt along side of it and aren’t on top of their monthly spending.

That’s their real source of stress and arguments.

Plus, they feel guilty spending money and aren’t really able to enjoy vacations or other things they feel like they should.

Paying off debt not only strengthens the family finances, more importantly, it strengthens family relationships.

Comparing debt repayment strategies & why the one you choose doesn’t matter

There’s a lot of talk out there about the debt snowball method vs the debt avalanche method.

It can actually get quite polarizing (needlessly in my opinion).

On one side, you have your financial optimizers who say that you pay off the highest interest debt first since it is the most expensive.

On the other side, you have those who like the debt snowball where you pay off the smallest debt first to get some momentum.

No matter which debt repayment strategy you choose to pay off your debt, you always continue to roll the debt payments to the next one on the list after you pay it off.

Which one should you choose?

Well, it’s easy.

Choose the strategy that most resonates with you.

Whether you start with the debt with the highest interest rates or the lowest balance, it doesn’t really matter.

Why?

Two reasons:

- There is little difference in cost between the two strategies when you look at a normal debt situation for a household.

- The most important thing is that you GET IT DONE.

What you don’t want, is to choose a strategy you think you should use, but you’re not that into it so you don’t follow it at all.

(Wait Rob, you said there’s little difference in cost. How is that possible, because paying off high interest debts first should save money).

I’m glad you brought that back up.

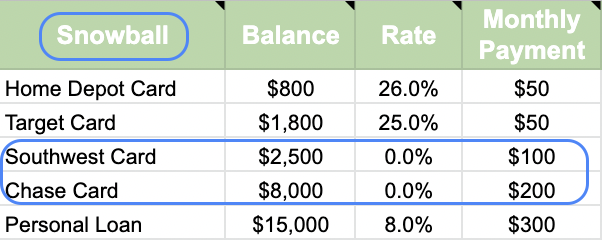

Here’s why with very common example:

- Home Depot – $800 – 26%

- Target – $1,800 – 25%

- Southwest card – $2,500 – 22%

- Chase card – $8,000 – 18%

- Personal loan – $15,000 – 8%

Notice anything interesting?

The lowest credit card balance also has the highest interest rate. That means no matter which method you use, you actually pay it off in the same order.

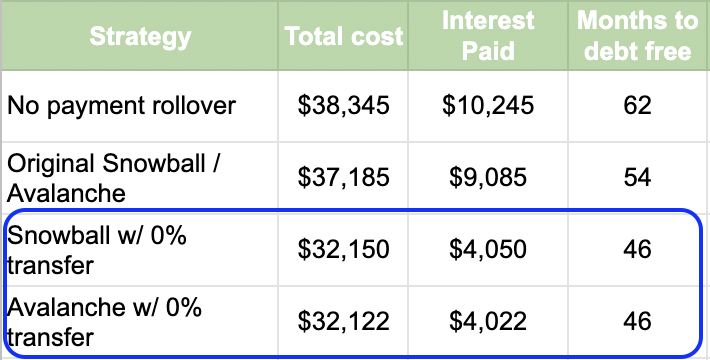

What we do know is that rolling over the payment to the next debt does lead to faster and less costly debt payoff.

Over the years, I have taken many client situations and run it in both ways. They mostly line up very similarly. Yes, the highest interest rate debt that a household carries is also usually the smallest balance.

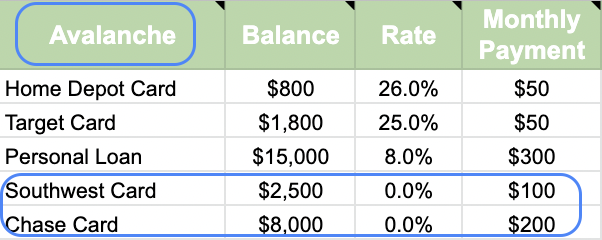

How does 0% credit card balance transfer compare?

Now let’s examine what happens to the avalanche and snowball numbers if we do a 0% balance transfer of the Chase Credit Card and Southwest Credit Card?

Here’s the original debt snowball order which stays the same even with the transfer:

And here’s how it changes with the avalanche:

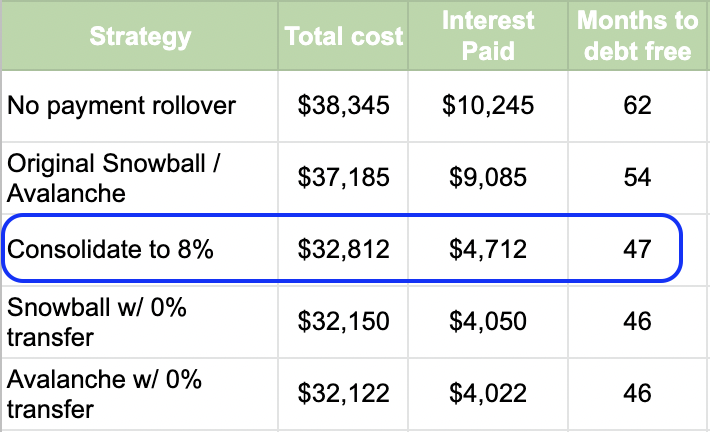

Surprisingly, the difference is minimal, less than the cost of a dinner date.

Here’s what’s for certain though, the interest rate reduction is amazing if they can keep rolling over to 0% for a few years.

It saves 8 months and ~$5,000 of interest cost.

That just goes to show how bad credit card interest is. It’s an extra $5,000 that could be in your pocket!

Given that they are so close, we must move next to the more important factor, freeing up cash flow.

What about doing debt consolidation?

Debt consolidation is when you roll all of your debts into a single loan with a single payment.

It is often used to transfer credit card debt to a personal loan with a lower interest rate.

So what would happen if they consolidated all of their credit card balances into one personal loan, going from multiple debts to one, going from 4 credit cards to 1 consolidation loan?

We’ll assume they are putting the same $700 per month toward paying off their debt, $400 on the consolidation loan and $300 on the prior personal loan.

As you can see, it saves more money than keeping the original cards, but not as much as the 0% transfer.

This again illustrates that the interest rate on the debt is important. However the order you pay it back in doesn’t really change much.

The most effective way to eliminate credit card debt

After all of that shifting and moving around, being dependent on your credit score and filling out paperwork, there’s actually a method that works much better than any of those…

Finding more money each month to pay off the debt. Ready for this?

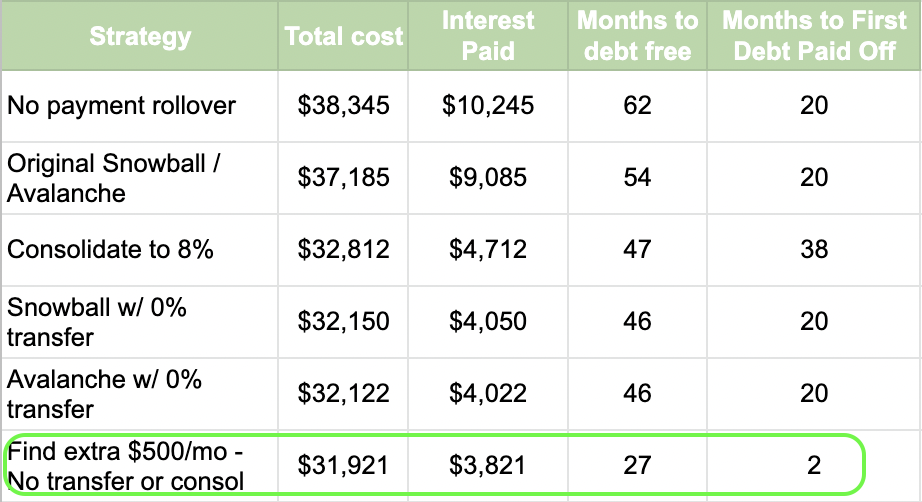

Here’s what it looks like if you went above the minimum payments and put an extra $500 every month toward your debts WITHOUT 0% balance transfers or debt consolidation.

That beats ALL other strategies alone.

- It shaves 2+ years off of the original debt avalanche and debt snowball method.

- It saves $5,264 (58%) on interest expense

- The first debt is paid off in 2 months instead of 20!

Now you might be thinking, “How am I going to come up with an extra $500 per month?”

Sometimes it’s a little bit here and a little bit there to find the extra money needed.

You don’t even have to take on a side hustle or get really great at your budget to make it happen.

Three are easy ways to cut your spending a little bit or you can even take some of that automated savings money and put it towards the debt.

Free up cash flow to stay out of debt

When debt payments take up a lot of cash flow, it’s tough to get ahead and stay ahead.

As we talked about earlier, reducing your monthly payments gives you more flexibility when you need it.

In this example, the last debt on the list comes with a $300 minimum payment each month, but the snowball made the actual payment $1,000.

If you have some extra expenses for the month, it’s ok to downshift a little bit to the minimum payment.

But when you have all the debt, there is no flexibility because those bills have to be paid or else you get hit with late fees, interest, and it knocks your credit score.

So it’s either miss a payment or take on more debt.

How to jumpstart your faster debt payoff

Here’s a step by step plan to get there.

Step 1: DON’T START BUDGETING

That’s right, I said it. You don’t need to start a budget as your first step.

Why not?

Well, simply put, it’s probably the hardest thing to implement, so people just don’t do it.

Let’s take some easier steps first to get momentum.

Step 2: Make a list of your debt, interest rates, and minimum payments

The first step is laying it all on the table.

You might dread doing this, but I can tell you that the clarity of knowing what you have to work towards is empowering. All of my clients say so.

Make sure you add in the minimum payment and the interest rate. If you can’t easily find the rate, just pick 20%. It might be a little higher or lower, but the most important thing is just to get this step done.

Step 3: Put the debt in order of how you want to pay it off.

Remember, this is not the most important step, but just pick what resonates with you.

Order your debt from smallest to largest or highest interest rate to lowest interest rate.

A different way I like to do it is based upon how quickly the debt will be paid off. Put the fastest one at the top and the slowest one at the bottom.

Simply divide the total debt by the monthly payment. List it from lowest number to highest.

(If you really love spreadsheets, put all the factors in and use the “nper” equation to create the order.)

What ends up happening is that you sprint your way to the finish line with the debt that you are closest to paying off.

I call it the Debt Sprint.

Again, it doesn’t really matter a ton financially, so just pick one that feels best.

Step 4: What resources do you have to throw a chunk toward the debt

Is there extra money sitting around somewhere that you can use to pay off a credit card or two? Perhaps in a bank account or idle cash in a brokerage account?

You don’t have to bring it down to $0, but think about how much you’d be willing to use to pay off debt.

Many people I work with can piece together some money to pay off the first debt on the list and sometimes the second one too.

There you have it. Interest saved, cash flow freed up.

Progress with the click of a button.

Step 5: Reallocate money going towards savings, investing, and debt

Rather than spreading out money to many different buckets and not filling any of them up, it’s time to get more focused.

REMEMBER: Paying off debt builds your net worth too.

Sometimes it can actually build it at a faster rate than if you were saving it or investing it, so it’s ok to move around where that money is going.

Here are some places to look to move money around:

- Automatic transfers to a savings account, another bank account, or money market.

- Paying more than the minimum on your mortgage, student loans or other debt not at the top of your list.

- Transfers to a brokerage account or college savings plans.

- Reduce your retirement plan contribution to only get the full match.

- Do you get a tax refund? Increase your take home pay by adjusting your withholdings.

The idea here is focus.

Keep money going towards consumer debt and get the max match from your employer retirement plan if they offer it.

All else is fair game.

Step 6: Explore 0% balance transfer and debt consolidation loans if it will significantly lower your interest rate

Most articles start here, but this is down the list in my opinion.

Why? Well, because the other stuff is more predictive of getting out of debt faster.

It will take some work to get out, but simply lowering the interest rate isn’t enough (though it is helpful).

Bonus tip: Try calling your credit card company and see if they’ll just simply lower your interest rate. Sometimes this works and is much easier than moving it around.

Step 7: Review your spending weekly

So often we wait until the calendar turns or we get the credit card bill to see where we end up.

But by then it’s too late.

If you review your spending weekly, you’ll have 4 opportunities to adjust your spending so you end up on target.

Plus you’ll know.

If you want a place to set your weekly budget, here’s a free template for you:

Step 8: Take at least half of any extra money to pay down debt

Get a raise, bonus, or tax refund?

You don’t have to use an “all spend” or “all save” mindset.

As long as you take at least 50% of it and apply it to paying off debt faster, you can do what you want with the rest.

This also helps with lifestyle creep. I call it the 50/50 Rule.

Paying off debt faster is easier if you have a plan

There are three things to take away from this:

- The biggest factor in how fast to get out of debt is how much extra you have to put towards it so the goal is to find more of it.

- Prioritize freeing up cash flow ahead of paying off high interest rate debt. Don’t combine everything into one loan if you can help it. The monthly payment relief and crossing a debt of the list is incredibly important to sustainability of the plan.

- Crossing the finish line is better than starting off hot and heavy and giving up. It will be a process, so make sure you measure progress, celebrate the victories, and spend on fun things too.

If you want to get anywhere with your finances and get rid of a major relationship stressor, pay off your debt faster.

It will give you the biggest bang for your buck.

Need help getting your debt in order or finding extra money?

Paying down debt is so much easier when you have a plan. If you find these tips helpful but want to make sure you have all the ways to pay off debt faster, schedule a free consult with me.

We’ll be able to talk through your specific situation and get you even more tools to dramatically improve your financial situation.

For informational and educational purposes only. Information was previously posted by Rob Bertman, Family Budget Services, formally Family Budget Expert, prior to Mr. Bertman joining Focus Partners. The opinions expressed may not accurately reflect those of Focus Partners.