8 Ways to Simplify Your Budget

Budgeting does not have to be complicated. You don’t have to have the perfect budget or the perfect system.

In fact, when you simplify your budget, you are much more likely to stick to it.

The best system isn’t nearly as good as one that actually works for you.

I’ll take you through some of the best ways to simplify things so you can spend less, save money and reach your financial goals.

Table of Contents

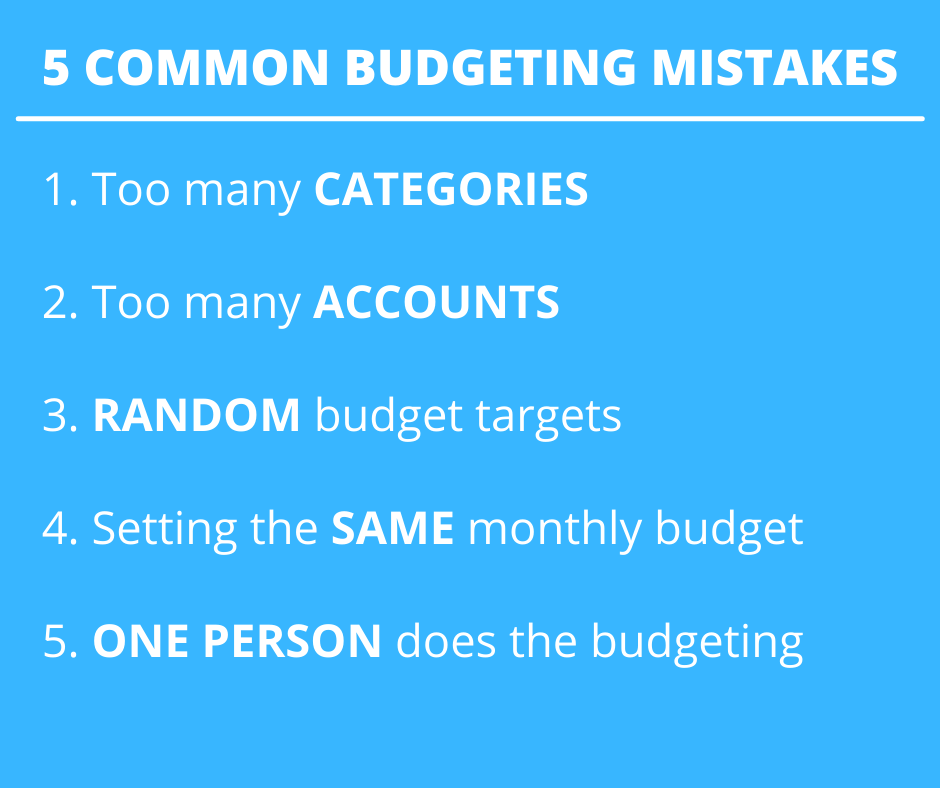

Top 5 Budgeting Mistakes I See

I’ve worked with hundreds of clients and have seen similar patterns which have led their budget to fail.

Let’s take a look at the mistakes before diving into how to simplify your budget.

Too many budget categories

The intentions are good here. But at the end of the day, too many budget categories clouds our focus.

For example, why do we need a budget for our mortgage or rent?

Our housing payment is typically fixed for a long time. It will never go over budget nor be under budget, so why do we need to track it?

Yes, it’s typically one of the largest expenses for families, but it can be accounted for in different ways.

Less is definitely more here.

Too many accounts

The more accounts we have, the more places we have to review to see what’s going on with our financial situation.

I totally get it if you have a bunch of investment accounts – IRAs, college savings plans, 401ks, brokerage accounts, etc. These accounts need to be separate due to the constraints around each one.

But the more checking and savings accounts you have, the harder it is to track your overall expenses.

Plus, it always seems there are a whole bunch of transfers going in and out. Each transfer is a line item that makes it hard to see the actual monthly expenses.

See if you can eliminate an account here or account there to simplify things.

Picking random budget targets

One of the main things clients tell me is that they don’t know where their money is going each month.

It’s very common.

When I ask them to guess, their actual total spending ends up being much higher than they originally thought.

Then, when you combine not knowing how much you spend each month with trying to create a budget, it becomes a recipe for failing at budgeting.

Can you cut your budget by $1,000? Maybe. Can you cut it by $3,000? That’s much harder!

They are called “spending habits” for a reason. They are ingrained in us and hard to break. To cut our expenses dramatically means changing up our comfortable routines.

So if we have to dramatically cut our spending, it means breaking a ton of habits – which grocery store we go to (or which groceries to buy), cooking more at home, cutting back on clothing and entertainment, less Amazon purchases.

When we underestimate how much we spend then double down by creating a budget with those underlying assumptions, the budget ends up requiring us to change drastically.

We don’t realize we committed to cutting that deep which is why we end up with much higher expenses than we budgeted for.

Thinking spending will be the same every month

“Something always seems to come up that takes us off track.”

This is another really common thing clients say to me.

Every month will be different. There are irregular expenses, things that happen each year, but not every month – birthdays, anniversaries, holidays, taxes, vacations, summer camp.

Keeping a static monthly budget throughout the year just isn’t realistic.

There’s something different every month that will come up as expected or unexpected.

Some months will be more expensive than others and budgeting needs to account for that.

One person sets the budget

This is a huge creator of financial stress (and marital stress) that I see with couples.

One spouse or partner sets the numbers but doesn’t involve the other.

Then all of a sudden, out of nowhere, they get upset with how much the other is spending.

But how would they know if they’re spending too much money?

There’s also the tug of war between, “How come you get to spend money on xyz, but you get upset with me?”

Expectations are set with one but the other has no context for those decisions.

Both need to be involved in order to avoid these arguments over money.

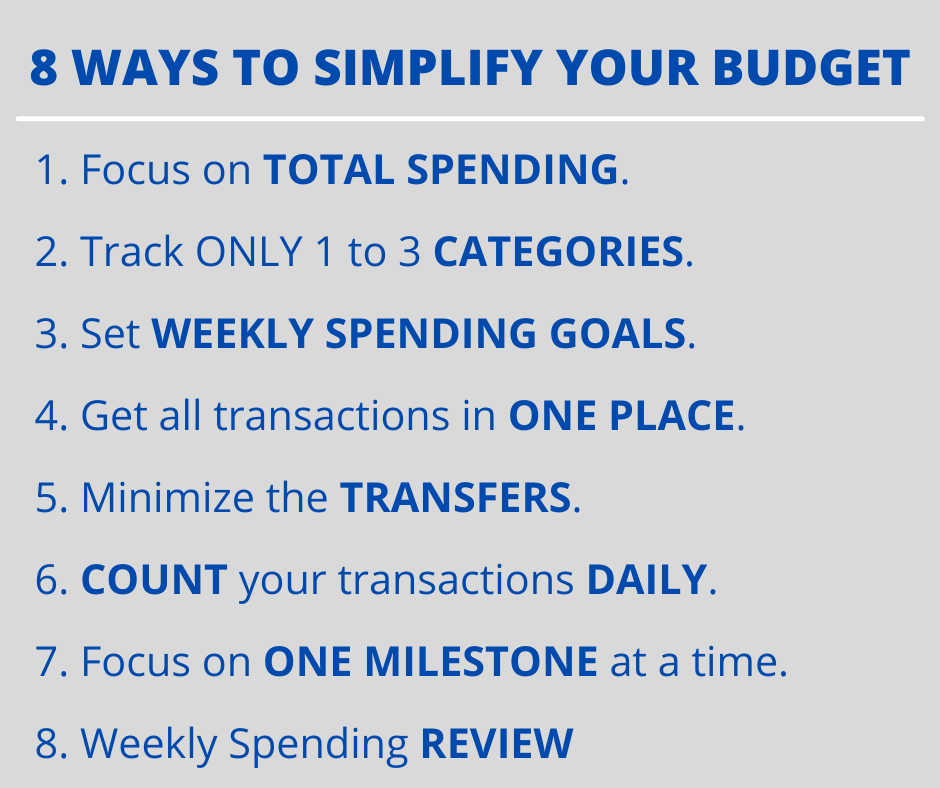

How to Simplify Your Budget – 8 tips

If you finally want to see your savings account grow, your credit card debt go down, and have more money to invest, it starts by setting a budget.

Better yet, simplifying your budget will make it much more likely to stick.

Here are 8 tips to simplify your budget.

Focus on total spending

At the end of the day, having more money left over is all about how much is going out vs coming in.

Looking at all of the budget categories can help you refine where your money is going, but by simply focusing on the total outflow, it makes it much easier to track.

If you only track one stat, this is the most telling and most important one to pay attention to.

Track only the 1 or 2 budget categories that you want to improve

In my mind, the purpose of tracking a budget category is because you actually want to monitor how much you’re spending and do better there.

So if you feel like the amount of money you spend on Amazon or dining out is getting out of hand, create a budget category to track spending only in that area.

Avoid the urge to track more than 3. Keep it to one or two budget categories if possible.

Everything else will be tracked by looking at your overall expenses for the month.

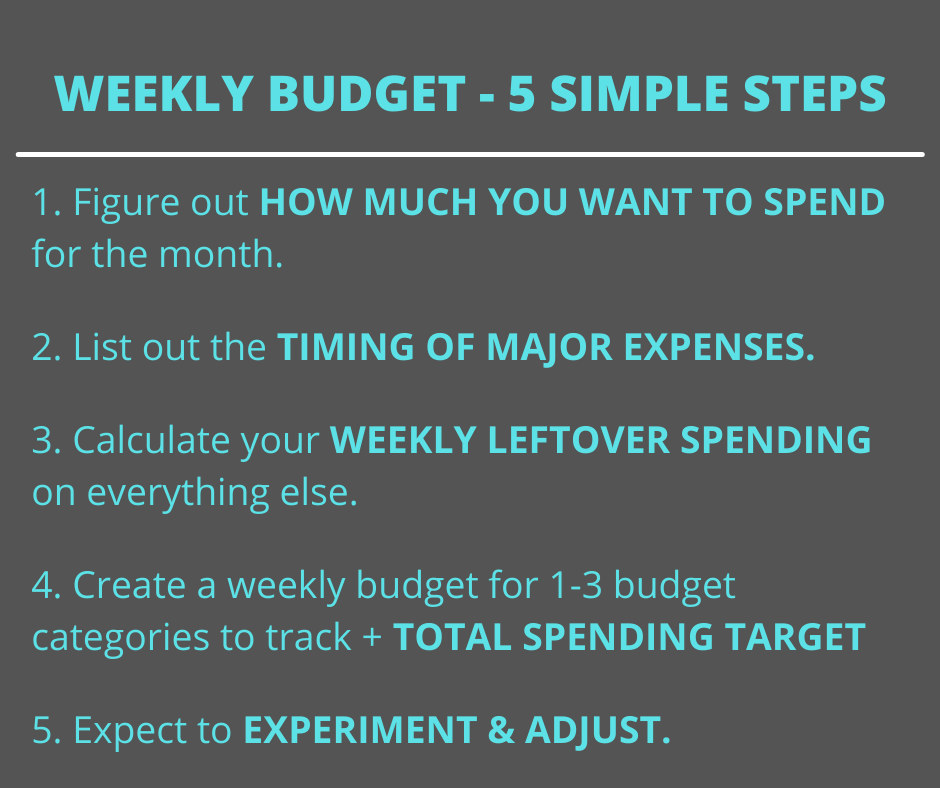

Set weekly spending goals

One of the best things you can do to stay on track is to set a weekly budget.

All you have to do is break down your monthly budget into weekly goals.

Week 1 will normally have the most money leaving your checking account because of your housing payment and possibly car payment.

Spread out the remainder to the rest of the weeks. Be sure to include other major expenses or irregular expenses that might pop up that week.

Get all of your transactions in one place

Whether you use a budgeting app or have your own spreadsheet method, you’ll want all of your expense data in one place.

The goal is to track how much you’ve spent whether you use cash, credit cards, a debit card, Venmo or Cash App.

The super simple way to see the total money you’ve spent is to add up your bank account balances then subtract how much you owe on your credit cards.

Be sure to add back any transfers to outside investment accounts

Stop all the transfers

This goes back to getting rid of excess accounts.

It’s hard to see what every little transfer is, whether it’s from one bank account to another, to your kid’s debit cards or to/from Venmo.

Wait to do it once a month or get rid of it altogether.

Minimizing how many times you do it will really help you simplify your finances.

Count your transactions each day

If you really want to simplify your budget (and your financial life), it gets no easier than just counting how many times you spend each day.

The most common reason people have trouble trying to save money is that the little things add up over time.

I can easily understand when clients are in this situation by simply counting the line items or their transactions.

If it’s 5 or more per day, they can easily reduce their spending by counting every time they pay for something.

Don’t worry about how much money is paid or automatic payments or bills that are withdrawn from your account, just focus on how many times you are spending money.

Go to the grocery store? That’s one. Buy something online? That’s two. Fill up the car with gas? That’s three. Have coffee with friends or co-workers? That’s four. Rent a movie or download an app on Apple? That’s five.

Budget 4 or less transactions per day. Don’t worry about the money being spent.

Focus on one milestone at a time

When we have too many financial goals, it’s hard to know what having extra money left over will do for us.

We’re much more likely to buy the thing in front of us than we are to consider which of the 20 long term financial goals we’d put that extra money towards.

But if you keep it simple and focus on one milestone at a time, it makes the choice to spend money or not much more clear.

Would you rather buy that item or work on getting to one more month in your emergency fund, pay off one particular credit card, or fund your Roth IRA for the month?

Not all three, which ONE?

With focus comes clarity to make the best decision for your current and future finances.

Monitor your weekly spending…together

Remember how we set weekly goals?

Let’s review them together by taking only 5 minutes per week to do it.

My Weekly Spending Review involves only 2 to 3 steps.

Simply (1) scan down your transactions then (2) look at your overall spending for the month.

(3) If you want to tack on the 1 to 3 budget categories to review, you can do that too.

At first, this might take more than 5 minutes, but as you get better at it, it will get easier and shorter.

You must do this together!

If one or both of you wants to do some work behind the scenes of categorizing or tracking where you’re at, that’s totally fine, but you should spend that 5 minutes together weekly.

This will make sure you’re both on the same page, know your numbers, and get you more comfortable with talking through it.

Need help simplifying your budget?

Try not to get overwhelmed by committing to do every single thing on this list.

Start by picking the number one tip that you feel will work best for you.

I suggest committing to the weekly spending review if you haven’t done so already.

This is what I do everyday and all day. I help families get better at budgeting, find ways to simplify, help them spend in alignment with their values while spending less and saving more.

All while getting along and arguing less about money.

If you want to learn more about how we can work together, click the button below.

For informational and educational purposes only. Information was previously posted by Rob Bertman, Family Budget Services, formally Family Budget Expert, prior to Mr. Bertman joining Focus Partners. The opinions expressed may not accurately reflect those of Focus Partners.