How to Create a Personal Balance Sheet – Learn the key info most people leave out – Example included

“That which is measured improves. That which is measured and reported improves exponentially” – Pearson’s Law

Enter the personal balance sheet. If you’re tired of working hard and having nothing to show for it, this is the way to measure (and then improve) your financial position and net worth.

I’ll also share the important information most people leave out that will help you make decisions on whether to save, invest or pay off debt.

Table of Contents

What is a personal balance sheet?

A personal balance sheet is a list of everything you own and everything you owe (aka your assets and liabilities) at this very moment all on one sheet.

It’s the way to organize your finances and make sure you’re aware of where all of your money is and that you’re staying on top of all of your debt.

Your balance sheet should also equip you with the info you need to improve your financial situation by understanding what’s helping or hurting your cause.

That’s the info most people miss, but you won’t. More on that later in the article.

Your balance sheet also calculates your net worth. What does net worth mean?

Net worth is similar to home equity. When someone sells their house, the check they walk away with after paying off their mortgage is the equity.

Now imagine you were to sell or liquidate everything you had of value and pay off all the debt you have. What’s left over is your net worth.

Net worth = Assets – Liabilities

Net worth is just like home equity except it’s ALL of your assets minus ALL of your debt.

Why is net worth important?

Net worth is your ticket to financial freedom and independence. It creates the cash flow to cover your expenses if you don’t have any income coming in from a job or your business.

A small-scale example would be an emergency fund.

Imagine that two separate families each spend $8,000 a month. Family 1 has $8,000 in a savings account. Family 2 has a $96,000 emergency fund. Neither of them has any other assets or debt (let’s keep it simple).

Family 1 could last only one month without income before draining their savings. Family 2 could cover their expenses for 12 months.

Having an emergency fund means being able to live the same lifestyle without any income. Financial independence is when you have a high enough net worth to live your life without having to rely on any income.

That’s why net worth is primarily what matters for financial independence. What also matters is the growth of your assets vs. your debt.

When assets go up, so does net worth. When debt goes down, net worth goes up as well. Yes, you can build your wealth by paying off debt.

Need help finding extra money to put towards your net worth?

How to create a personal balance sheet

If you want to increase your net worth, you need to start tracking your net worth, so let’s get to measuring and reporting by putting together your personal balance sheet.

Creating a balance sheet will take six steps. Then I’ll show you how to interpret what it means and the keys to improving it.

Step 1: Make a list of your ASSETS and where to get the most current values.

Here’s a list of things you might own by category. Assets include:

- Immediate access

- Savings account

- Checking account

- Non-retirement investments / brokerage account

- Revocable trust

- Retirement accounts

- Employer retirement accounts – 401k, 403b, 457

- IRA – Traditional, Rollover, Roth, SEP

- Pension / Profit sharing plan

- Accounts for kids

- 529 plan

- Educational IRA

- Custodial accounts

- Business ownership

- Company stock

- Ownership stake in your business or another

- Private equity

- Real estate

- Primary residence

- Vacation property

- Investment property

- Complicated assets

- Cash value life insurance

- Irrevocable trust (if you’re the beneficiary)

- Inherited IRA

- Collectibles of value

- Vehicles (unless leased)

Notate where you can find the information about the current value. It could be through an online account, your most recent statement, or with a phone call.

Step 2: Make a list of your DEBTS and where to get the most current values.

When we talk about money owed to others, we need three key pieces of info:

- Amount owed

- Interest rate

- Monthly payment

Keep that in mind when you’re thinking about where to get the information on your debt. Most of this information can be found through our online account or most recent statement.

The hardest part will be to find the interest rate on some of these debts, but it’s really important to get that info.

Here’s a broad list of liabilities or debts you might owe:

- Credit card balances

- Past due bills

- Back taxes owed to IRS

- Auto loan (or future lease payments added up).

- Federal student loans (Stafford, Grad PLUS, Parent PLUS)

- Private student loans

- Property loans

- Mortgage

- Home equity loan

- HELOC (home equity line of credit)

- Personal loans owed to a bank or financial institution

- Financed purchases (furniture, appliances, electronics, cell phone)

- Line of credit

- Money owed to family or friends

If you want to take this a step further, check your credit report to see if you missed anything.

Now you have your list! Time to get the info.

Step 3: Compile the information.

Now that you have your checklist of what you need and where to find it, let’s go get it!

This process could take about 30 minutes or so, because you have to track down your most recent statement, search through your emails, login to accounts whose passwords you may have forgotten, and maybe make a phone call or send an email or two.

That’s ok! Take the time to do it. Make it a game to complete your checklist as fast as possible.

Remember that you’ll want the most recent values, interest rates on your debt, and any monthly payments you’re required to make.

Most other financial experts will only give you these steps in their “how to prepare balance sheet” articles.

But now comes a more critical part if you want to actually understand what all of this means.

Getting it all in one place will feel like such a relief, and things get easier from here. I promise. 🙂

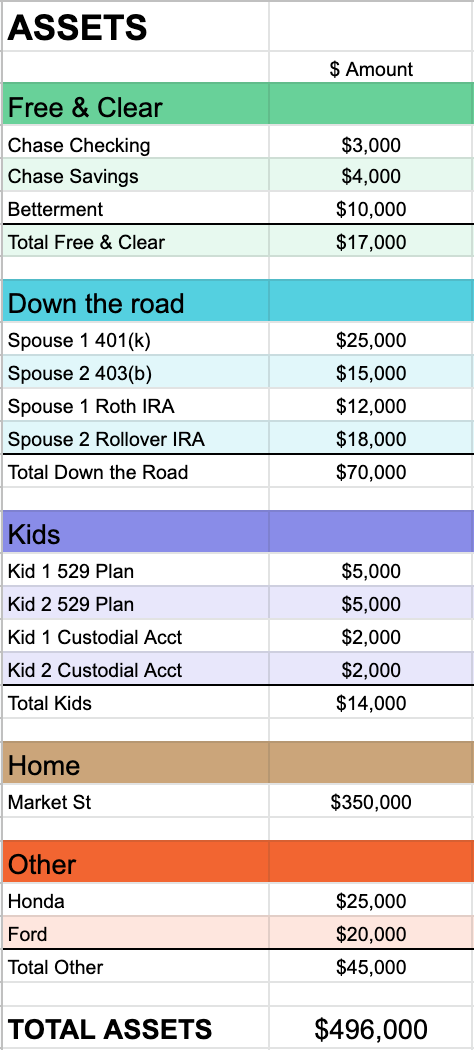

Step 4: Categorize your total assets

Let’s take all the good stuff and put it in an easy-to-understand format. The way I like to do this is by when or how I can access the money.

- Free & clear funds (aka liquid assets) – You can get to the money within a week without restrictions.

- Checking & savings accounts

- Non-retirement investment accounts

- Vested company stock

- Down the road (aka retirement accounts) – Can’t access until you’re 60 without penalties.

- Employer retirement plans (401k, 403b, etc.)

- IRAs

- Pension

- Company stock (not vested)

- Kids – Any account to benefit your kids

- 529 plans

- Custodial accounts

- Home

- Other hard-to-sell assets

- Vehicles

- Investment properties

- Ownership stake in a business

- Collectibles

- Cash value life insurance

- Irrevocable trust (if you’re the beneficiary)

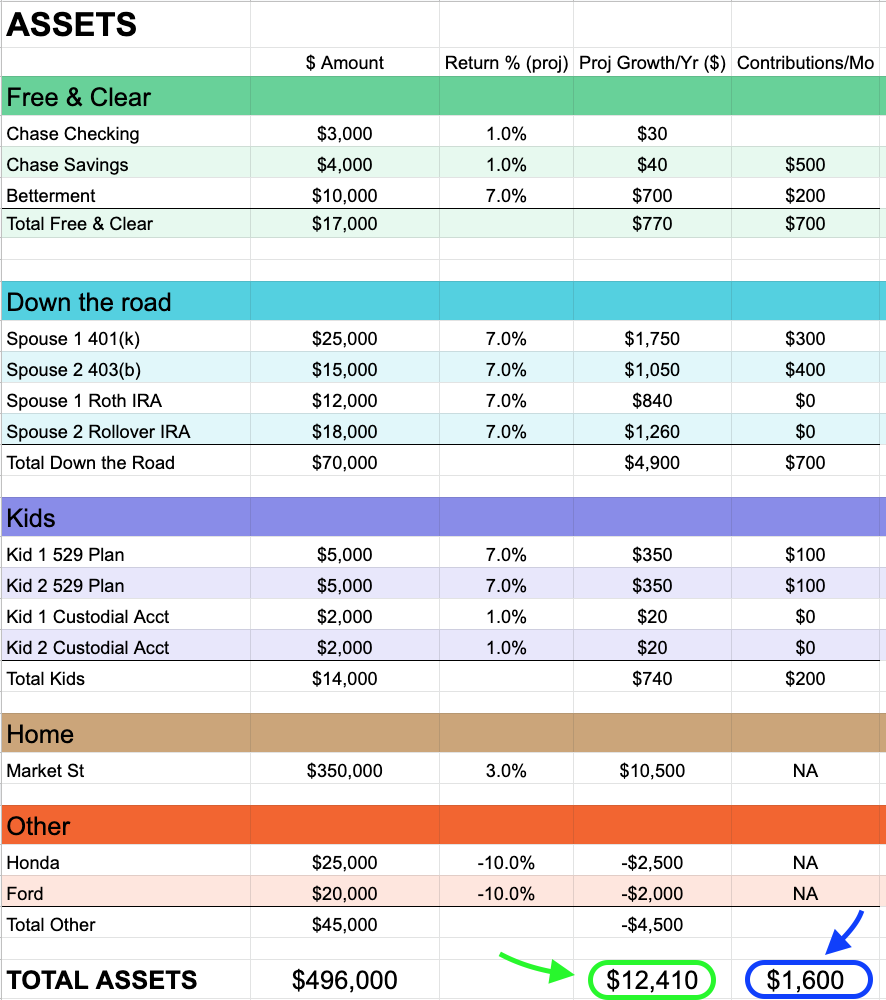

Here’s an example of what it might look like once they’re organized by these categories:

This number has a “feel good” context to it, because this is the value of things we can see, touch and feel.

Also, most people are thinking about the day-to-day accounts in the “free & clear” section. When it’s tight there, it can feel like you’re broke.

After seeing how much they have spread around to other things like retirement assets and their house, they usually feel better.

Organizing your assets like this can also help you identify where your financial stress is coming from.

Take a look at your numbers in each category. What becomes the priority for you?

Building up your emergency fund? Feel like you’re behind in retirement and it’s time to up your game? Are your cars the best asset you have?

Once you pinpoint the source of stress, you are more motivated to change it.

Remember though, this side of the equation doesn’t take into account the debt, which is why it also feels good to look at it.

Debt comes next for us.

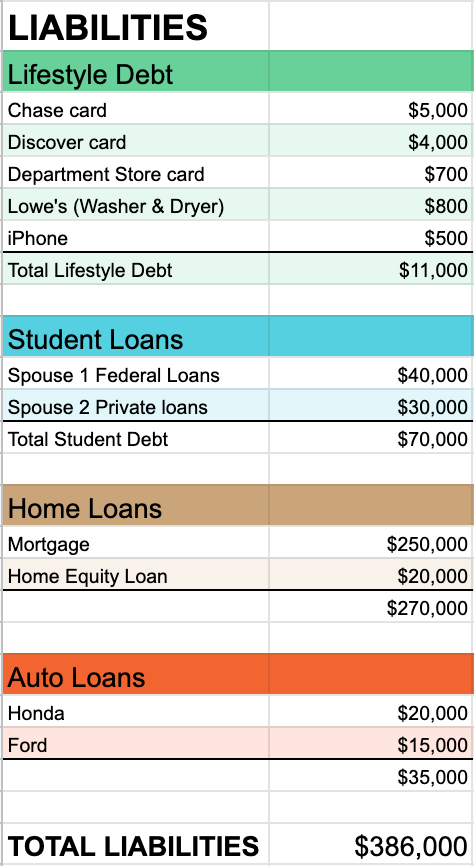

Step 5: Categorize your total liabilities / debts.

If I’m being honest, this is the not-so-fun part. We collect and add up everything we owe to other people.

I’ve mentioned to my kids, “You can see the joy of what people have, but you can’t see the stress of what they owe.”

Translated: You can see people’s assets but not their debt.

My clients often feel some hesitation getting all of their debt information together, but once they have the clarity of their debt situation and put it into an easy-to-understand format, it becomes a motivation for action.

The way I like to categorize debt is based upon how it was accumulated and if it was borrowed to buy an asset. Here are the categories I use.

- Lifestyle debt:

- Credit card debt

- Past-due bills

- Personal loans owed to a bank or financial institution

- Line of credit

- Financed purchases (appliances, furniture, electronics, cell phone)

- Student loans

- Federal student loans (Stafford, Grad PLUS, Parent PLUS)

- Private student loans

- Auto loan (or future lease payments added up).

- Home loans

- Mortgage

- Home equity loan

- HELOC (home equity line of credit)

- Money owed to family or friends

- Back taxes owed to IRS

- Other debt

- Investment real estate debt

- Loan against cash value life insurance

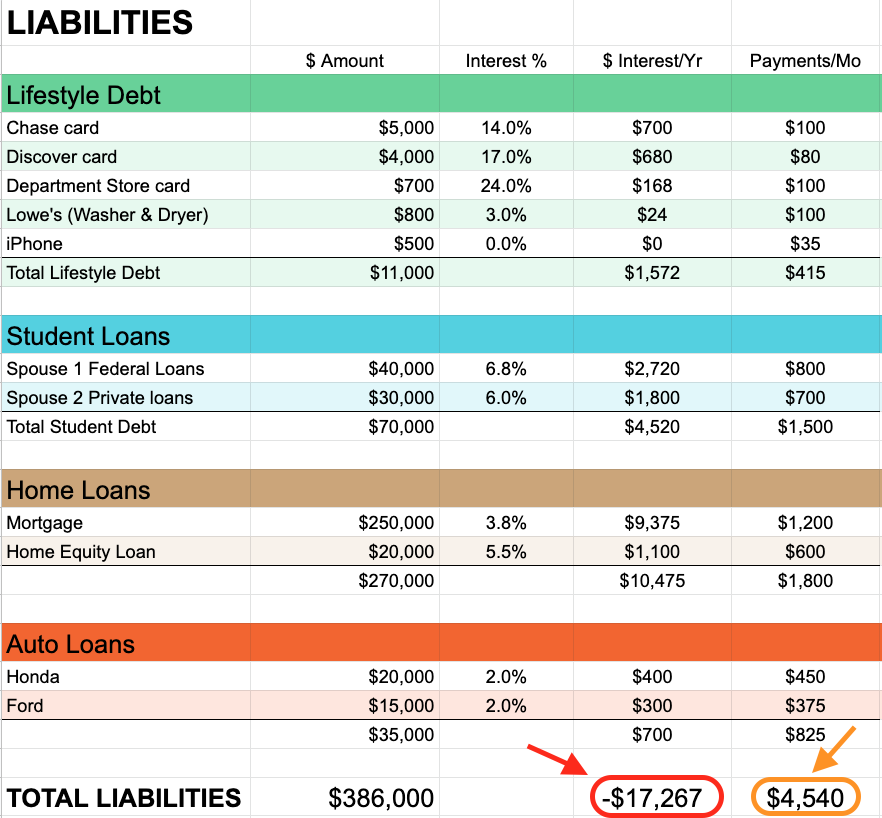

Here’s an example of total liabilities organized by these categories:

Step 6: Calculate your net worth

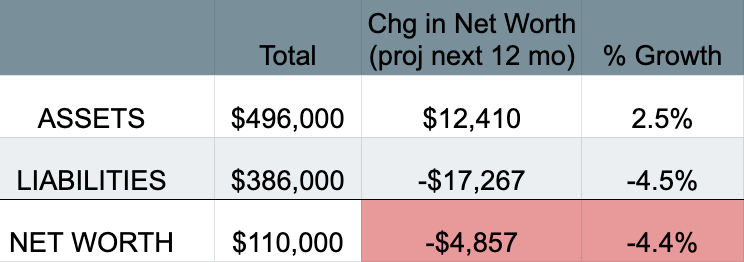

Calculating your net worth is a simple calculation now that you have this info. Take your total assets minus your total liabilities.

In this example, we’d take $496,000 – $386,000. That equals a net worth of $110,000.

Most people feel better about their situation when they see their true net worth, which captures their entire picture.

However, I’ve worked with many clients who have a negative net worth (they owe more than they have). Many times, it’s a result of six-figure student debt.

No matter where you stand today…

Your current net worth is not representative of your financial future.

REMEMBER Pearson’s Law: You are measuring it and reporting it so you can improve it exponentially.

Please know that if you’re feeling stressed and want expert help for your specific situation, I’m here for you. No strings attached.

Personal balance sheet example

Now let’s see what it looks like when we put it all together:

*Fun fact: Notice we put the assets on one side, the liabilities on the other side along with the net worth and the values “balance”. $496,000 in assets on one side and a total of $496,000 in liabilities and net worth on the other side. That’s how balance sheet got its name.

Voila! Your personal balance sheet…

Wait, what do you do now?

How do you use this information to make wise choices about improving your net worth?

Flaws of the traditional balance sheet

The traditional balance sheet doesn’t really tell you what to do, so I have come up with some other items to add so that you can actually understand what you’re looking at and where to make changes.

Here are some common questions I get from clients and readers that a normal balance sheet only vaguely answers:

- Should I save, invest or pay off debt?

- When should I use cash to pay off credit card debt?

- I have a decent amount in retirement but still feel like I’m behind. Why do I feel this way?

- I feel like I don’t spend that much money, so how come I feel like I’m juggling bills and living paycheck-to-paycheck?

To be fair, there are other personal financial statements that help with this. One is called a “cash flow statement” which helps track cash inflow and outflow), but honestly, it’s complicated and I know very few people who do this for their personal finances.

But what if we could put key information all in one document so you can be informed of the next great move?

Key information missing from a personal balance sheet

We want to build your wealth efficiently and also understand the context of when/how we can access it.

We also want to know how paying off a debt or adding to an investment would help our cause. In other words, how do we prioritize what to do with our money?

Here’s a list of the info we’ll need to add to the balance sheet. I had you collect most of this this when you were compiling the info:

- Assets

- Monthly contributions to savings, retirement accounts and other investments

- Projected returns on assets

- Liabilities

- Interest rate on debt

- Monthly debt payments

- Net worth

- Net worth by when/how you can access it

- How would your net worth change if you didn’t pay off any debt or save / invest any more money?

Project your asset growth

The asset side of the balance sheet will change based upon how its values change over time and also how much extra cash is going towards saving and investing.

Most assets will go up in value over time (appreciating assets), while some will go down (depreciating assets).

On my personal balance sheet, I use default rates of return as my projections:

- 7% for investment / retirement accounts, mutual funds, ETFs, stocks

- 3% for real estate

- 1% for cash

- -10% for vehicles since they depreciate about that much each year

*Anything can happen in any one year and over time, so these default rates of return are just estimates.

Here’s what the asset side will look like once we include these rates of return and monthly contributions:

There are two key pieces of info here:

- Now we can see that $1,600/month in cash ($19,200 per year) is going toward growing assets.

- We can see that the assets are projected to grow by $12,410 on their own over the next year (again, just an estimate).

Taking those two numbers together, it looks like total asset growth is projected to be $31,610.

Clearly see problematic debt

You may have heard the terms “good debt” (like a mortgage) and “bad debt” (like credit card debt). Let me just say I disagree with those blanket terms.

Debt is bad if it’s ruining your financial position. For example, a mortgage is not “good debt” if it’s making you house poor.

Two key factors in determining toxic debt are interest rate & monthly payment, so we’ll want to capture these in the balance sheet. The higher either of those factors are, the worse the debt is to your financial picture.

Let’s add your monthly payments and interest rates to the liabilities side of the balance sheet:

Now this gives us some real insight into why someone might feel stuck in the mud and the stress that comes with it.

- $4,540 per month is going toward debt. Nearly $55,000 of this couple’s take home pay is going to debt each year! That can be crippling!

- About $17,267 is being lost to interest this year, a horrible impact on net worth. About $1,500 has to go toward debt each month just to stop it from growing.

Using these numbers, 2e can project that they’ll pay off approximately $37,213 in debt this year (total payments minus projected interest).

The majority of the debt pay down is student loans and the auto loans.

Now let’s take a look at how the assets and liabilities interact with each other.

Personal return on net worth – What is it and why did I make it up?

Personal return on net worth (PRONW) is the key to financial independence.

Net worth is important, but it’s what your net worth is projected to do if you didn’t have any income or salary coming in from work. Can it sustain you? How is it performing?

This may get a little technical, but bear with me.

In business, there’s something similar called “return on equity” (ROE – not the kind that comes on sushi). It measures how well a company is generating income compared to its net worth.

You take the net income of a company (income minus expenses) and divide it by its shareholders’ equity (which is the same calculation: net worth = assets minus liabilities).

High ROE is a sign of company strength and competitive advantage. It is earning good money compared to how it is capitalized.

A high PRONW means that your net worth is very optimized and growing on its own.

ROE uses net income, but PRONW uses the projected growth of your net worth if no debt was paid down and no more money was saved.

Let’s go back to our example and take the total assets, debt and the projected change of both sides:

Simply put, the interest charges on the debt are higher than the projected asset growth so this example shows a negative PRONW- not very efficient.

This is not uncommon for many people, but it also shows us that the debt is hindering this financial situation.

So what can we do? Let’s get a little more granular.

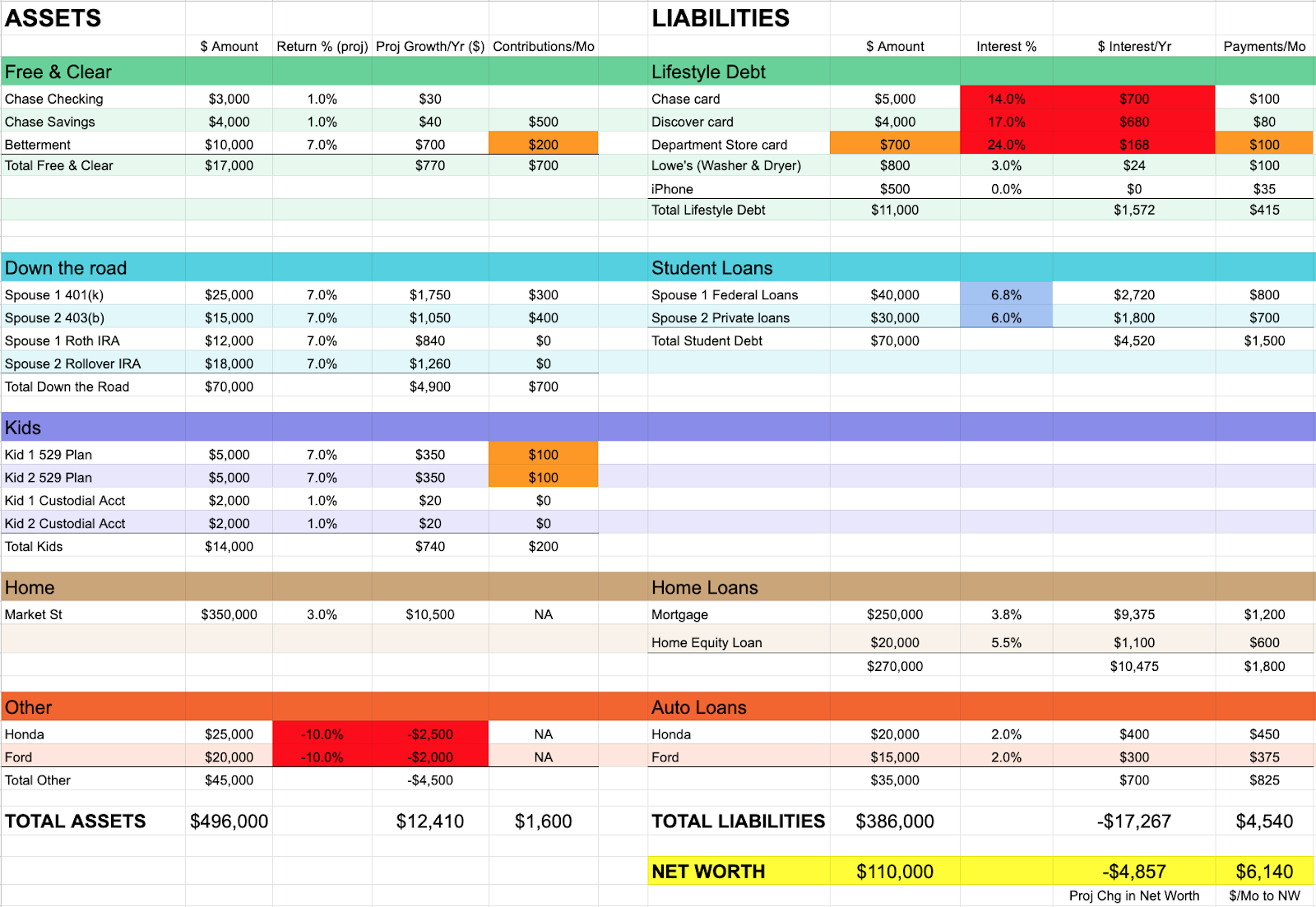

How to make your personal balance sheet more efficient

In order to fix this, we need to prioritize the things that are penalizing net worth, see what we can move around, and focus cash flow on what is hurting net worth the most until it is eliminated.

*None of the changes I’m about to show have anything to do with budgeting or saving more money. This is just shifting things around that you’re doing currently.

The red areas are real trouble (credit card debt & the cars). The orange areas are opportunities to shift cash flow around to optimize wealth over time. The blue are possible refinancing cases.

Yes, the cars are in red, but I’m not suggesting selling them unless they can’t keep up with payments and bills. We don’t have to go crazy here.

It does show what can happen to your net worth if you have a bunch of money tied up in cars. The price of the car is more important to your net worth than the interest rate on the car loan.

*FYI, car leases are much worse than owning a car and having car payments. We won’t get into that here, but don’t lease.

What else can we do?

- Let’s pay off the $700 department store card immediately – an instant 24% return on investment.

- Then, let’s shift the money going to Betterment and the kids’ 529 plans to accelerate paying off the credit card debt. That will give them an extra $500/month to pay those off. It’s better to pay off 17% and 14% interest rate debt compared to investing it.

- Refinance private student loans. In this case, it makes sense to refinance the federal student loans as well because loan forgiveness isn’t an option. Let’s say they can lower their interest rate to 4%.

*Federal student loans operate by much different rules than all other debt. If you have six-figure student debt, hold off on refinancing until you check out Student Loan Planner.

What do those changes result in?

- Immediately save an estimated $2,000 per year in interest expense.

- Credit card debt goes from being paid off in seven+ years to ~1 year.

- We still keep the $500 per month going toward building an emergency fund for security.

That is a wild improvement without having to find more money in a budget to put toward these goals!

Tracking your net worth improves your financial position

Remember Pearson’s Law?

Thanks to calculating net worth, they’ll be credit card debt-free, have a $12,000 emergency fund, and free up an extra $680 per month that was going toward debt in just…one…year! Way to go!

Now you can see that adding the extra factors of monthly contributions and payments as well as interest rates and expected returns puts all the information we need to make positive changes in one place even without having to save more money.

Need a personal balance sheet template?

You can get instant access to my personal balance sheet template right here.

Please also email me if you have any questions whatsoever. I’m here to help!

By the way, I’m always available for a free 30-minute chat also.

For informational and educational purposes only. Information was previously posted by Rob Bertman, Family Budget Services, formally Family Budget Expert, prior to Mr. Bertman joining Focus Partners. The opinions expressed may not accurately reflect those of Focus Partners.