Pay off Debt or Invest? Your 8-Step Guide

What happens when you have to make a choice between 10 different options?

Nothing…well, procrastination happens…unless you put it off 🙂

The more choices you have, the harder it is to choose. So we end up suffering from analysis paralysis and just doing nothing at all.

“Should I pay off debt or invest?” It seems like a simple question.

“But wait, there are so many choices with investing and paying back debt! What should I do?”

“Ahhh! I’m overwhelmed! I’ll figure it out later…”

Not only does overwhelm keep us from making progress, we spend more money and have less left over because we haven’t figured out the purpose of having an extra $1 left over.

But once you know where your money needs to go, creating a budget is motivating. You now be excited about the progress you’ll make with the extra cash you can free up.

Let’s go from being overwhelmed to having clarity!

I’m going to lay out a pay off debt or invest roadmap for you.

But first let’s talk about why it’s important to both get out of debt and invest for the future.

Table of Contents

Why pay off debt?

Debt is money that you’ve spent, but you haven’t paid for it yet.

If you have debt, you’re not alone.

Total consumer debt is $14.9 trillion according to debt.org. That includes auto loans, credit cards, student loans, and mortgages.

So what are the benefits of paying off debt?

It frees up cash flow.

The average family spends more than $12,000 per year on debt payments.

That means that the first $18,000 of salary per year (pre-tax) is going right towards debt.

What would you do with an $18,000 raise? You’d probably put it towards your financial goals like buying a house, retirement, taking family vacations, or saving kids’ college.

So when we pay down debt, we give ourselves a raise because that cash flow is now freed up.

It gives you a return on investment

This might be a new perspective for you.

The interest rate on the debt you pay off = your return on investment.

Think about it.

When you carry credit card debt with a high interest rate of 20%, you are giving the bank a 20% return on investment. The bank is earning that return off of you.

When you pay off debt, you are taking that return away from the bank which means that you are mathematically earning that return on every extra dollar of principal you pay down.

Not only that, but it’s a guaranteed, risk-free, tax-free investment return given to you immediately when you pay down the principal balance of a loan.

That’s hard to beat!

It increases your net worth

Did you know that paying down debt actually builds wealth?

When you look at your personal balance sheet, your net worth is what you get when you add up the assets and subtract the liabilities.

Paying down debt moves that negative number closer to zero which has a positive impact on your net worth.

Think of it like the equity you have in your home. If your house is worth $500,000 and you owe $400,000, you have $100,000 in home equity.

$500,000 home value – $400,000 mortgage loan = $100,000 home equity

But if you pay down your mortgage balance by $100,000, your home equity increased by the $100,000 of debt you paid down

$500,000 – $300,000 = $200,000

The first thing we think of when we talk about building wealth is growing our assets. But, paying down debt builds wealth too.

Why invest?

When we look at the balance sheet, investing is the positive side while debt is the negative side.

That’s true both in how to calculate net worth and also the mindset around each side.

Investing is exciting! You get to put money away and watch it grow and the upside seems endless (especially in a hot stock market).

Debt on the other hand is something we don’t really want to look at.

There are so many great reasons to invest, so I’ll focus on just the main ones.

Compound interest

Albert Einstein and Warren Buffett both have great quotes on the power of compound interest.

Einstein called it, “the eighth wonder of the world” and Buffett credits being it (along with living in America & having good genes for his massive wealth.

I remember watching an old science tv show when I was a kid and they had a very powerful demonstration of the power of compound interest.

The question was, “Would you rather have $1,000,000 or start off with 1 penny that doubles in value every month?”

Seems obvious to take the $1,000,000, but you can sense there’s a catch…and there is.

How long would take to reach $1,000,000 if a penny doubles every month? The answer will amaze you.

It takes somewhere between 26 and 27…years? No…27 MONTHS!

How about $10,000,000? Well that takes 30…MONTHS! From a penny!!

Investments won’t compound at that pace but a moderate 7% return means your money will double every 10 years. After 20 years, you’ll have 4x. 30 years, 8x, 40 years, 16x, 50 years, 32x.

Your money works for you

The power of compounding means it’s best to get started early, but it’s also never too late.

If you stuff $1 under a mattress, it will still be $1 when you pull it out, but if you invest it, every $1 you put in will work for you.

For example, if you’re starting from $0 and put $1,000 per month away using dollar cost averaging and it earns an annualized return of 7%, here’s how your money would grow:

The hard work you had to do to come up with that $1 extra will pay off, because that $1 will now multiply by investing it..

Financial independence is living off of your investments

To reach financial independence, you’ll need assets to support you.

You can live off the interest / investment returns, dip into the principal balance, or a combination of the two.

But the bottom line is that you need assets to draw on to support your cost of living so you can achieve financial independence.

Is it better to pay off debt or invest?

Let me cut to the chase here…

Paying off debt and investing are the same thing!

Remember that paying down debt means that you are earning that investment return back from the bank or lender.

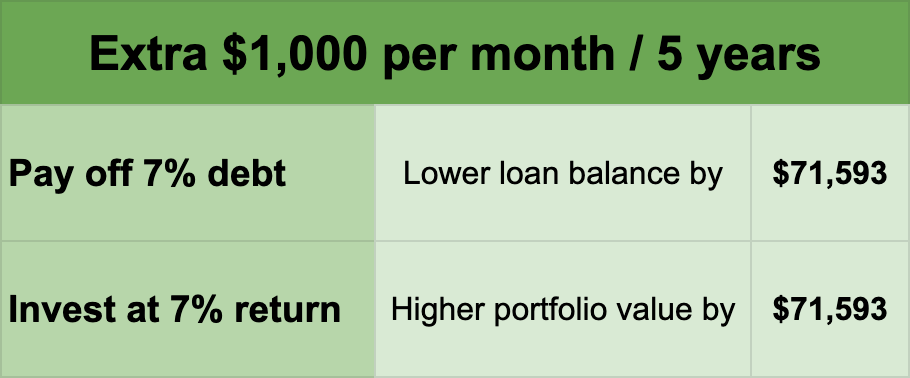

For example, let’s say that you had an extra $1,000 per month and you could choose to pay down the principal on a debt with an interest rate at 7% or invest in something that would grow by 7% per year for 5 years.

Where do you end up?

*The extra monthly payments toward the debt are in addition to the minimum payment. All extra money goes toward paying down the principal balance.

Your net worth ends up in the same spot! +$71,593.

But in my mind, paying down high interest rate debt beats investing because:

- Paying off debt frees up that cash flow.

- Investing to reach a 7% investment return requires taking some risk.

- Paying off debt improves your credit score so you can apply for lower interest rates through refinancing.

But you don’t have to go all in on getting out of debt or all in with your investments. Some investments will beat paying down certain debts and vice versa.

So then how do you prioritize which debt to pay before investing or what investing to do before tackling debt?

Before we dive into that, let me just answer one more common question I get.

Is it better to pay off debt or save money?

Some of my clients are uncomfortable using savings to pay off credit card debt, and that’s ok.

Sure, it’s a mathematical no-brainer to take $5,000 from a bank account earning 0.5% to pay off a $5,000 store credit card at 25%.

That money in the bank would earn interest of $25 of interest, but paying down the card saves them $1,000.

Saving (along with paying down debt and investing) is an important piece of where to put extra money.

Saving money can actually be better than paying off debt (despite the math) for these reasons.

It helps you feel secure

If you don’t feel secure, it’s hard to think about anything else.

Some people want to have money in the bank because it feels good. That comforting feeling allows them the mental space to take action on other goals…like paying off debt.

If that sounds like you, keep one month of expenses in a checking account as a starter emergency fund while paying off credit card debt.

Even though it’s not the most efficient thing, do what will help you feel ok throwing everything else at credit card debt with high interest rates.

Emergency savings keeps you from getting back into debt

I had one client tell me recently that they had eliminated just about all of their credit card debt. But then something happened and they had to go back into debt to stay afloat.

That’s where a cash cushion comes in.

Having an emergency fund makes sure that you stay out of debt even with surprise events.

Ok, back to investing vs paying off debt.

How to prioritize investing and paying back debt

“If I had extra cash, where could I get the best bang for my buck?” Should I pay off debt or invest?

Now that we know the the interest rate on debt is the same as earning that return on investment, we can easily see what to do.

Step 1 – Get the max employer match from your retirement plan

The greater the match, the more compelling it is to get the max.

For example, if your employer match is 50%, then every $1 you put in up to the full match will earn you 50% off the bat then an investment return after that.

Find these details about your plan. If your employer doesn’t offer a matching program or it’s minimal, then skip this step.

Step 2 – Pay off credit card debt

Credit card debt is typically the highest interest rate debt you could have (aside from other predatory loans).

Store credit cards usually have the highest interest rates (20%+) and people usually carry the lowest balance compared to traditional bank credit cards through Mastercard, Visa or Discover so it’s usually best to pay those off first.

You can choose the debt snowball (lowest balance to highest balance), debt avalanche (highest interest rate to lowest interest rate), or another method that suits you.

Again, the interest rate on your card is the rate of return you would earn back. Getting a 20% risk free return is pretty much unbeatable!

Side note: Pay off 0% cards too because eventually the rate will go up. Plus credit card debt is the gateway drug to financial ruin. Pay it all off and never carry a balance again.

Step 3 – Tackle High Interest Debt

High interest debt could include personal loans, a home equity line of credit (HELOC), and even some auto loans.

In my mind, any debt that has a rate of 5% or more should be paid off next, especially since bond rates and savings rates are so low.

Why do this before investing? The stock market has historically returned 8-10% but there’s a lot of risk and volatility that goes into that, so I’d take the guaranteed return to pay off debt.

Step 4 – High stress debt

We all have that debt we just can’t stand that we owe. Maybe it fits into one of the above categories, but maybe it doesn’t.

High stress debt includes money owed to family members, friends, or back taxes owed to the IRS or your state’s department of revenue.

It could also be that auto loan you don’t like making payments on or another payment that just irks you everytime you see it leave your checking account.

Forget about the interest rate and just get rid of it, and feel your stress level melt away!

Step 5 – Roth IRA & Brokerage Account

Now we’re back to investing! The goal is to earn a 7-10% annualized return over time.

You have now freed up extra cash by getting rid of monthly debt payments and making the most efficient use of your money.

If you’re eligible to make a Roth IRA contribution, it’s one of the best investment accounts out there because of how it’s taxed. If you’re above the limit, you can explore a Backdoor Roth Contribution but check with your tax advisor before jumping ahead.

As for the brokerage account, there’s no limit to how much you can put in and how much you can withdraw. It’s like a savings account but one where you can invest.

The downside is that this is a taxable account meaning that you’ll have to pay taxes on income, dividends, and capital gains along the way.

But the tradeoff is your flexibility in how you can access the funds. You’ll trade short term volatility with higher returns and growth over the long term.

Step 6 – Max out retirement plan

Now we finally get back around to maxing out your employer retirement plan and maxing it out.

If you have a Roth option through work like a Roth 401(k) or Roth 403(b), then you can skip the Roth IRA from the last step and contribute to the retirement plan instead.

Step 7 – Pay off all debt except for you mortgage

Here’s where we clean up the debt side of your balance sheet.

Get rid of all low interest debt, payment plans, etc.

Imagine the feeling of having no debt payments outside of your mortgage.

Step 8 – Pay extra on your mortgage

Phew! You made it.

The mortgage usually has the lowest interest rate and takes the longest to pay off. It’s for those reasons that we tackle this after doing everything else.

Now pay off your house early and feel the benefits of living debt-free!

What about student loans?

You might think student debt should be taken care of in one of the above steps, but that’s not necessarily the case.

You can refinance your student loans to get a lower interest rate possibly in the 2-4% range. It’s a good idea to explore refinancing private student loans especially. Then it belongs in Step 7.

If you have federal student loans and owe more than you make, then an income driven repayment plan with loan forgiveness might be a better option for you. In that case, student loan debt would come after Step 8, super low priority.

Not sure what to do with your student loans? Check out Student Loan Planner for free calculators and resources or get a custom student loan plan.

Should I invest or pay off debt? Summary

Where will you get the biggest bang for your buck? Now you know.

This should be like a waterfall. Pay the minimum on everything and fill up these buckets one at a time.

But always remember that the best plan for you is the plan that you connect with and suits YOU.

A simple, focused plan that resonates with you will ensure you make progress. It might also entice you to find ways to free up other cash since you now know where it’s going to go.

If this is something you want to take to the next level, then book a free session with me so we can identify where you need help and how to best get it.

Want help freeing up money so you can pay off debt and invest, but you don’t want to talk just yet? Download my free guide.

For informational and educational purposes only. Information was previously posted by Rob Bertman, Family Budget Services, formally Family Budget Expert, prior to Mr. Bertman joining Focus Partners. The opinions expressed may not accurately reflect those of Focus Partners.