Budgeting to pay off debt (without changing your lifestyle)

We would all love to find extra money at the end of the month to put towards paying off debt.

But there’s always some challenge that comes up.

Either we can’t get the budget to stick or an unexpected expense comes up or it’s hard to stay motivated to make it to the finish line.

But budgeting to pay off debt does work if you know how to remove the obstacles and keep stoking the fire to get there.

We’ll take you through why getting rid of debt can be challenging, the popular debt repayment strategies, and how to find extra money at the end of the month to pay it down.

Are you ready? Let’s dive in!

Table of Contents

What is debt?

The classic definition of debt is when money is borrowed and owed back to the lender.

That’s a very jargony definition that doesn’t really bring it home for our reality.

So I define debt differently.

“Debt is money spent that you haven’t paid for yet.”

Why do I define it this way?

To remind us all that consumer debt (like credit card debt) comes from spending money but not having the funds to pay for it.

It’s not free money. We still have to pay it back at some point.

The danger comes when we have to play catch up as well as support our lifestyle going forward.

Why is having debt a bad thing?

No judgment here. Some seasons of life mean going into debt and that’s ok.

But at some point it should be paid back as quickly as possible.

Why is debt so bad?

Debt makes everything you buy more expensive

Most debt carries an interest rate. That means you end up paying back more than you borrowed in the first place.

The two biggest factors that make it more expensive are the interest rate and how long it takes for you to pay it off.

Let’s say you spend $1,000 on various things throughout the month.

If you pay cash, it costs you…$1,000.

But if you put it on a credit card at 18% and it takes you 12 months to pay it off, then it costs you $1,100. If you pay it off over 2 years, then it costs you ~$1,200.

Nothing changed about when you got it, but now you’re paying 10%-20% more for the same thing.

Even if you get a 0% balance transfer, that still typically has a 3% fee attached to it, so it costs you $1,030 to pay it back.

Debt eats up your cash flow and raises your monthly expenses.

We still need to spend on things we need to get each month.

But when you carry debt, you are buying the things you need today and also playing catch up on paying back what you’ve spent in the past.

(Graphic of paying for money already spent and also the things you need today.)

I call this payment stacking.

It’s when you rack up so many monthly payments that you don’t have the room to cover your current expenses.

The faster you catch up, the faster you get rid of payments and lower your monthly expenses.

Being in debt is like always playing catch up

Ever feel like you have so much to do that you may never catch up?

You finally work through it, make a ton of progress, and almost get caught up. Then all of a sudden a project or event comes out of nowhere.

Being in debt is like being in the hamster wheel. It feels like you’re spinning your wheels and going nowhere.

When you take on debt, you now have to play catch up while also maintaining your current expenses.

Why is paying off debt so hard?

Paying off debt is so hard, right?

Just when we make progress, we revert back to where we were before.

Why does this always seem to happen?

Yes, some of it can be that major financial things come up that sidetrack us. But could it be other things outside of money?

Here are major non-numbers factors that make it hard to pay off debt.

We get used to it

Let’s face it. For as much as we want something, it can often feel easier to maintain the status quo than to make changes.

Part of that problem is that we try to make all these drastic changes at the same time. But if we take our time and make gradual changes, it becomes much more sustainable.

Think, The Tortoise & The Hare.

Whenever we try something new, reversion back towards what we’re used to will happen. That’s fine as long as we don’t slip all the way back.

Commit to improving your finances and raise your financial standards gradually.

Debt seems like an insurmountable amount we’ll never get out of.

There’s the saying about how to climb a mountain…one step at a time.

Being able to pay off your debt can seem like an audacious task, but take it little by little.

Any major goal should be broken down into smaller, more easily attainable, shorter-term goals.

Debt repayment is the same way.

Instead of focusing on getting out of debt, focus on getting out of one loan first.

That’s why methods like the debt snowball or debt avalanche are so effective. That focus on one small step at a time keeps you engaged.

Along with that, it’s important to not live in the gap as one of my mentors once told me.

It’s the idea of being so focused on the end result, that you forget to look back and see how far you’ve come.

We don’t want to live in the rear view mirror, but looking back to see progress keeps the momentum going.

We focus on our credit score instead of getting out of debt

Is a credit score important? Sure, especially if you need to qualify for lower interest rates.

Do you know the best way to improve your credit score? Pay down debt.

So don’t get distracted with that number.

Stay focused on the main mission, pay off your debt. Everything else will follow.

Not sure where to start – Too many choices

Long term goals don’t matter if you don’t figure out the very first action to take.

There’s a concept called “Goal Setting to The Now” where you break down the long term goals into the steps you need to in the next 5 years, 1 year, 6 months, 90 days…this week.

But that’s really hard to do if you have to sift through so many choices and get paralysis by analysis.

It’s best to make a choice and stay focused. Action beats optimization.

Whatever strategies you’ve read about, just pick the one that resonates most with you and get started!

Where will the extra money come from?

Great! So you have your plan in place and know what you need to do…but there’s one major roadblock people run into.

How will you come up with the extra funds to make it happen?

This is critical because it’s the fuel that will help you accelerate your way to paying off your debt.

Before we get there, it’s important to figure out where your money is going in the first place. So start by simply tracking your spending with a simple 5 minute weekly spending review.

Don’t try to budget or figure out how much more to put toward your payments until you understand where your money is going.

Need more help here?

You feel behind on investing

So many people I work with feel like they are way behind with their investing so they feel like they have to focus on that instead of paying down debt.

But did you know that when you put money toward debt, it is very similar to investing?

Whaaa?!?

Yes, paying down debt and investing have a lot in common.

First of all, both are net worth building activities.

Investing makes your assets go up and paying off your debts makes your liabilities go down. Both have a positive impact on your wealth.

But all things being equal, it’s better when you get out of debt because:

- You free up cash flow and lower your expenses

- That interest rate on a loan is a risk-free, tax-free rate of return on investment.

- Reduces stress and anxiety.

Whether you invest or pay off debt, it’s the same thing in a lot of cases.

Not on the same page about whether to save, invest or pay off debt

This is very common, and it’s an easier solution than you might think.

If one of you wants to focus on saving or investing instead of paying off debt, guess what?

You can do both!

Even for the most diametrically opposed mindsets around what to do with money, pick what resonates most with each of you and simultaneously work your way to each goal.

Then, focus all of your money on just one goal in each category.

If one of you wants to pay off credit cards and the other wants to max out their retirement plan, that’s great!

But in order to do that, focus all money on just those two items.

Don’t make extra payments on your mortgage, save for kids’ college, or anything else at the same time. Just work towards paying off your credit card balances while maxing out your retirement account.

You’ll get there faster and get rid of the biggest stressors or financial concerns.

You don’t have to get entirely on the same page with money, but you need to listen to the other’s perspective. Both are valid.

The most important thing is that you make progress…together.

How to pay off debt – Comparing 3 common strategies

The end goal is to become debt free, but how you choose to get there may impact how fast you get there and if you can keep your motivation.

You see, most people try to do everything all at once. That’s a mistake!

It’s best to break up your debt repayment and focus on one thing at a time.

This will keep you motivated as you work toward paying off debt and will free up extra cash flow along the way.

The methods are the debt snowball, the debt avalanche, and the spread out approach.

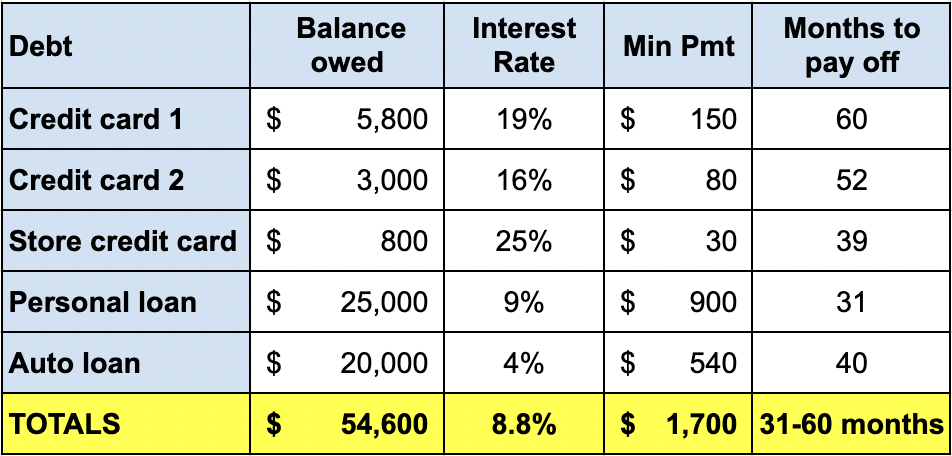

Here’s a hypothetical example of a household with debt. We’ll use this to compare/contrast the various debt payoff methodologies.

*FYI, I’m intentionally leaving student loans out of the example, because student loan repayment strategies can vary greatly based upon how much a household owes in student debt compared to how much they make and their eligibility for loan forgiveness. Plus, it doesn’t impact the results analysis.

Debt Snowball

The debt snowball method was made popular by Dave Ramsey. Whatever your opinion of him is, this method of paying back debt is extremely effective.

The idea here is that you order your debts from the smallest amount owed to the largest amount.

Then you focus on putting everything you can toward the smallest remaining debt while making minimum payments on everything else.

After you pay off a debt, you roll that payment to the next smallest debt and so on.

The debt snowball method is highly effective because it’s a very simple and easy to follow plan without a ton of analysis to the strategy.

You don’t have to search for the interest rates on all of your loans, and it helps you pay off that smallest debt very quickly to feel progress, celebrate, and build confidence that you can finish it out.

Debt Avalanche

The debt avalanche is a financially efficient and optimized debt repayment strategy.

It’s similar to the debt snowball in that you line up what you owe, focus on one at a time and make minimum payments on the rest. Then the debt payments roll to the next loan on the list.

But the order of debt payoff is based upon the interest rate rather than the amount.

Start by maximizing debt payments on the one with the highest interest rate until it’s paid off, then work your way down to the one with lower and lower interest rates.

The benefit to this is that you pay off the most costly high interest rate debts first (usually credit cards), then work on the lower interest rate debts last.

This makes sure you’re getting the very best return on every extra dollar you put towards on paying down your loan balances.

Make more than the minimum payment on all your debts at the same time

This is by far the most common starting point I see with clients.

The way it works is that you spread out the money going toward debt repayment around to pretty much all the debts at the same time.

Put an additional $100 per month here, $200 there, round up to the nearest round number on the mortgage.

Families may approach debt repayment this way because they want to feel like they’re doing a little bit extra everywhere and covering all their bases.

Progress is made using this approach which is the most important thing.

But, the problem with this method is that it’s actually takes longer paying off your debt and doesn’t give any quick wins.

Doing it this way can feel like a slog and like you’ll never become debt-free because you never see anything be fully paid off.

Comparison of the 3 debt repayment methods

Let’s take a look at the summary for each of these three methods using our example above.

We’ll first take a look at what the snowball and avalanche methods would look like if we just did the minimum payments.

The key takeaway here is that rolling over the monthly payments is extremely effective. It helps save money in interest and cuts nearly 2 years off of the timeline to becoming debt free.

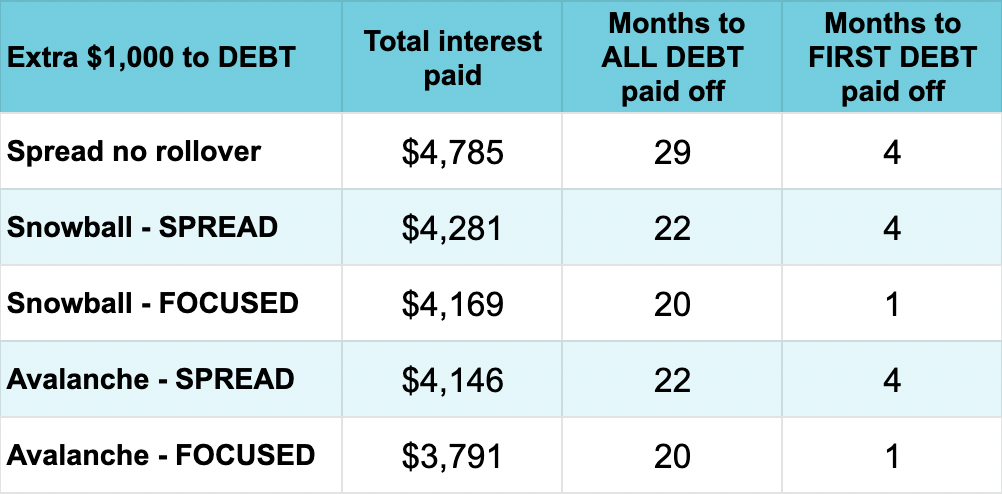

Now let’s look at what adding $1,000 to the monthly payments would do using 2 methods.

In one example, the $1,000 extra is spread out equally to the 5 loans

The first is spreading it out, $200 extra added to each of the 5 loans so all payments are more than the minimum payment.

The second is focusing the entire $1,000 on the debt at the top of the list while making minimum payments on all the others.

Comparing these debt repayment strategies is fascinating.

Spreading out the extra $1,000 to start is not nearly as effective as focusing it all on one of the debts at a time.

Probably the most surprising finding is that there is little difference in the debt snowball and avalanche from an interest savings perspective and no difference in how long it takes to become debt free.

That shouldn’t make sense though right? The avalanche method is geared toward saving the most on interest, so shouldn’t that be the result?

Yes, it should.

But the situation for most families is that credit cards usually have the highest interest rates and the lowest balances.

That means the order of the loans is very similar for both the avalanche and snowball methods which is way there isn’t a big difference in the numbers in the real world.

While student debt, personal loans, auto loans, debt consolidation loans may have high interest rates, the rates are normally way lower than credit card debt and fall further down in both the debt snowball and the debt avalanche.

There are two key takeaways from what this hypothetical example shows:

- It’s better to put all additional money focused on one debt at a time rather than spreading it out to everything.

- At the end of the day, what far and away matters most is how much you have to put towards all of your debts.

So let’s talk about how to free up more cash.

How to budget to pay off debt

Now we know that finding the extra cash to pay toward your debts can rapidly accelerate your way there, what’s the best way to do it?

Well, you might think you should create a budget first.

Nope!

Here are the 6 steps to take.

Step 1: Track your spending

Of all the financial habits to choose from in personal finance, tracking your spending is by far the most important one and the best place to start.

Why do you start there?

When I start working with clients, they are always wondering where they can cut their spending.

It’s hard to know the answer without tracking it first.

Plus, people drastically underestimate how much they’re spending.

Sure they can name their regular bills, the mortgage payment, the car payment, but the discretionary and one-off spending can be way off.

Start by signing up for a budgeting app like Mint or YNAB and add all accounts where you spend money (like credit cards, bank accounts, etc).

Step 2: Identify the things you want to keep spending money on

Aha! You probably thought I’d say cut spending.

So often we think we have to cut out everything including what we like doing or feel guilty about.

Nope, there are plenty of things to cut without giving up what we enjoy.

So start by thinking about what you want to keep spending on first, you non-negotiables.

You don’t have to give up everything you enjoy doing…or maybe even at all. It’s ok to spend money on yourself.

Plus, prioritizing what makes you feel your best makes it easier to stay the course.

Step 3: Make a list of all your debts

Grab the info you need to figure out what you need to tackle.

Make a list of anything you need to plan to pay back:

- Credit card balances

- Student loan debt

- Auto loan

- Mortgage

- Personal loans

- Lines of credit

- Money owed to family

Get information on each of the debts:

- Loan balance

- Minimum payment

- Current payment

- Interest rates on each of your debts

If you want, you can download my personal balance sheet template to help you through this process.

Step 4: Pick your debt repayment strategy

No need to get cute here whether you use the avalanche or snowball method, just pick the one that works best for you.

Stay focused on eliminating the one at the top of your list.

Step 5: Think about places you can easily reduce your spending without giving up what you enjoy

Now that you’ve been looking at where your money is going, and what you want to keep, you can more easily identify the things that don’t serve you and are a waste of money according to YOU.

Think of it as a choice between only two options. You can spend on something or put that money toward the first debt on the list.

Having a binary choice like that makes the spending cuts much more meaningful and tangible, because that money has a specific purpose if it’s not getting spent.

Look for the layups like unused items that you can cancel, negotiating lower monthly bills, cutting back on the things you enjoy but could spend less on, etc.

Step 6: Track your overall spending weekly

So often, we get caught up in the details and make things more complicated than they have to be.

Budgeting is simple.

Track only the numbers that you have control over or want to improve.

That means, looking at your total spending and the 1-3 budget categories you want to improve.

There’s no need to have a budget for your housing payment for example. It just gunks up your brain and doesn’t help at all. It’s a fixed expense that you can’t change unless you move.

Focus only on the key metrics that you can change if you wanted to.

When you’re reviewing your spending and budget weekly, you’ll have 4 weeks to adjust so that you end on target.

Need help with your budget to pay off debt?

Having a clear plan will help you pay back debt faster and feel good about it along the way so you can see it through.

Once the plan is in place, the best thing you can do is find the money at the end of the month to put towards it.

This is my specialty and I’m happy to help!

Set up a free consult with me and we can talk through how to make it happen!

For informational and educational purposes only. Information was previously posted by Rob Bertman, Family Budget Services, formally Family Budget Expert, prior to Mr. Bertman joining Focus Partners. The opinions expressed may not accurately reflect those of Focus Partners.